The strangest number in AI this week is not a context window, a benchmark score, or a GPU cluster size. It is 5 percent.

The OpenAI government stake proposal would give Washington a slice of the company behind ChatGPT, according to The Verge’s summary of Financial Times reporting. The reported stake would be worth about $42.6 billion if priced against OpenAI’s latest post-money valuation. OpenAI said on March 31, 2026 that it had closed a $122 billion funding round at an $852 billion valuation. That makes the proposal less like a public-relations coupon and more like a new line item in the AI economy: political equity.

For builders, the important part is the precedent. If frontier AI firms start paying for policy peace with equity, revenue shares, or access controls, your dependency graph now includes Congress, Commerce, Defense, and the White House. The API endpoint may stay the same. The risk model around it does not.

What did OpenAI reportedly put on the table?

OpenAI has discussed giving the US government a 5 percent ownership stake as a way to ease tensions with the Trump administration and answer public anger over who benefits from AI, according to The Verge’s July 2, 2026 report. Sam Altman reportedly argued that public ownership would let Americans share in AI’s upside, with the same idea potentially extended to other US AI companies.

The math is blunt. OpenAI’s own funding announcement put the company at $852 billion after its March 2026 round, so a 5 percent stake implies roughly $42.6 billion before any discount, restriction, or special share structure. The same OpenAI announcement said enterprise deployment represented more than 40 percent of revenue and was on track to reach parity with consumer revenue by the end of 2026.

That matters because the proposed stake is aimed at a company that has become infrastructure for other companies. ChatGPT is a product, but OpenAI’s API, enterprise tools, and agent stack sit inside workflows that other teams have already budgeted around. If the government becomes a shareholder, even a passive one, every enterprise buyer will ask a practical procurement question: who gets priority when public policy and customer needs collide?

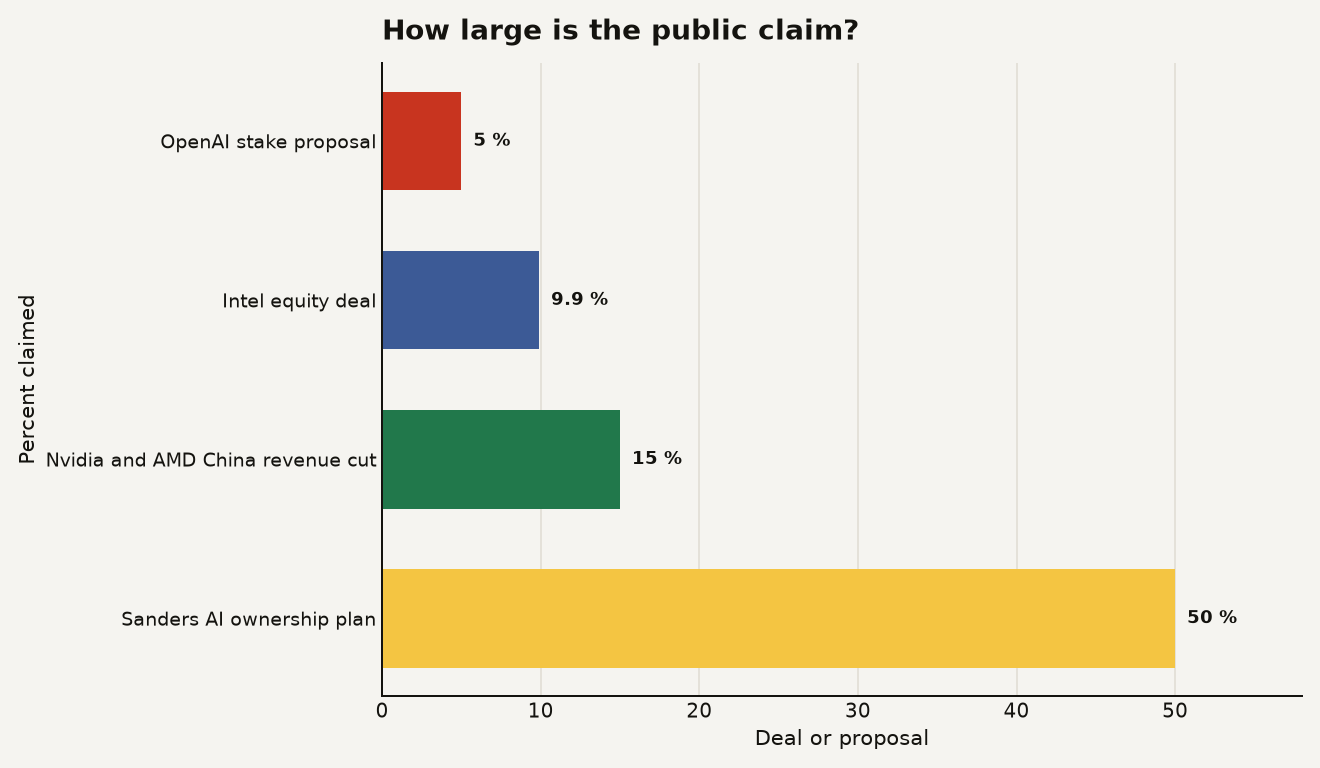

The chart below puts the OpenAI number beside other recent proposals and deals. OpenAI’s reported 5 percent stake is smaller than Intel’s 9.9 percent government deal, smaller than the 15 percent Nvidia and AMD China chip revenue share, and far smaller than Senator Bernie Sanders’ 50 percent public ownership proposal.

Intel said in August 2025 that the US government would buy 433.3 million primary shares at $20.47 each, equal to a 9.9 percent stake. AP reported in August 2025 that Nvidia and AMD agreed to share 15 percent of China chip-sale revenue with the US government to secure export licenses. Axios reported on June 18, 2026 that Sanders unveiled a plan for the government to take 50 percent equity stakes in large AI companies.

The policy menu is now visible: equity, revenue tolls, export controls, and release approvals. OpenAI is trying to choose the least painful version before someone else chooses for it.

Why would a frontier AI company want Washington on the cap table?

The obvious answer is protection. A government stake can turn a regulator into a financial beneficiary, which changes the temperature of every fight over data centers, model releases, labor disruption, and copyright. A 5 percent public stake also gives OpenAI a cleaner answer to the charge that AI profits accrue to a narrow ownership class while public data, public research, and public infrastructure carry part of the cost.

OpenAI has been laying groundwork for this argument. In its March 2026 funding post, the company said its inclusion in ARK Invest exchange-traded funds would broaden ownership and give more people the chance to share in the upside economics of OpenAI. In April 2026, OpenAI said its Stargate infrastructure push aimed to secure 10 gigawatts of US AI infrastructure by 2029. Those two claims belong together: the company wants to look like a national growth engine, not just a private model vendor with a very large power bill.

The political context is harsher than a normal antitrust debate. AP reported on June 26, 2026 that OpenAI restricted the release of a new model at the Trump administration’s request, while Anthropic received approval for only a limited release of its strongest cybersecurity model after federal intervention. AP also reported on July 1, 2026 that the administration lifted restrictions on Anthropic’s latest Claude models after a weekslong ban tied to cybersecurity concerns.

That is the builder’s warning label. Frontier model access is becoming a permissioned market. The trigger might be cybersecurity, export controls, defense procurement, or a deal that looks like a sovereign wealth fund. The result is the same for your roadmap: the model you plan around in Q3 can become a restricted model in Q4.

If you already treated model access as a product dependency after the GPT-5.6 delay permit race, this is the capital-structure version of the same problem. A government stake does not need a board seat to matter. It can matter through procurement pressure, export guidance, informal release review, and the threat of becoming the next company used as an example.

What does this change for builders buying or building on AI?

The underrated consequence is procurement drag. A startup choosing between OpenAI, Anthropic, Google, Meta, and open-weight models used to compare capability, latency, price, privacy, and lock-in. Now it also has to compare political exposure. That sounds abstract until a customer asks whether a model endpoint could be limited to government-approved users, or whether foreign employees may keep access during a sudden export-control review.

Here is the practical breakdown:

- Codebase risk: if your product depends on one frontier model for reasoning, code generation, or customer support, build a fallback path for at least one alternative provider in 2026.

- Roadmap risk: avoid promises that require a specific unreleased model, especially in regulated sectors like finance, defense, energy, and healthcare.

- Cost risk: policy tolls can show up as higher API prices, narrower model access, longer enterprise review cycles, or mandatory compliance features.

- Hiring risk: teams will need more policy-literate engineering leadership, because model governance is becoming part of systems design.

- Moat risk: if every frontier provider gets pulled into a public wealth or national-security bargain, the durable advantage shifts toward workflow data, evaluation harnesses, distribution, and customer trust.

The last point deserves the most attention. A 5 percent government stake does not make OpenAI’s models worse. It makes the model layer more political. When the model layer gets more political, the value of owning your evals, your retrieval layer, your data contracts, and your user workflows goes up.

This is where hype gets lazy. Public equity in AI is often framed as a moral debate about redistribution. That debate matters, but it is only one slice of the operational story. For a product team, the sharper question is whether a provider can keep shipping predictable capabilities under political supervision. A model that benchmarks well but arrives late, ships under a whitelist, or loses international access is a weaker dependency than its leaderboard score suggests.

What should you do before this becomes normal?

Start by treating frontier AI procurement like cloud procurement after the first big geopolitical outage. You do not need panic. You need boring resilience.

First, map your AI dependencies by blast radius. Which features fail if one provider is restricted for 7 days? Which customer promises fail if a model is unavailable outside the United States? Which internal tools handle sensitive code or vulnerability data that might draw extra scrutiny under future cybersecurity rules?

Second, separate model quality from release reliability. Your evaluation suite should score accuracy and latency, but it should also track portability: prompt compatibility, tool-call behavior, refusal patterns, data-retention terms, and regional access. If a fallback takes 6 weeks of prompt surgery, it is theater.

Third, make commercial terms carry policy risk. Enterprise AI contracts should ask for notice periods, model-substitution rights, data-export paths, and service credits tied to restricted access. If your vendor sells you frontier capability, it should also explain what happens when Commerce, Defense, or the White House asks for a narrower rollout.

Fourth, watch the structure of the OpenAI proposal more than the headline number. A passive 5 percent economic interest is one thing. Voting rights, information rights, release-review commitments, procurement preferences, or a broader industry pool would be far more consequential. The difference between a dividend claim and a control channel is the difference between a tax and a steering wheel.

The forward read is simple. AI companies will keep offering public-benefit structures because they need legitimacy at the same time they need more power, chips, water, land, and political patience. Governments will keep asking for a cut because AI looks like a national asset and a future tax problem in the same spreadsheet. Builders sit in the middle, paying for abstraction while the abstraction gets negotiated above their heads.

The API is gaining a toll booth

OpenAI’s reported 5 percent offer is small enough to look reasonable and large enough to prove the point. The frontier AI market is no longer just a race to better models. It is becoming a race to secure permission to deploy them.

If you build on top of that market, plan like a grown-up. Keep your model layer swappable. Keep your data portable. Keep your customers informed. The next AI shock may arrive as a policy memo, and it may cost more than latency.

Sources

- The Verge: OpenAI floats giving Trump administration 5 percent cut of AI boom

- OpenAI: OpenAI raises $122 billion to accelerate the next phase of AI

- OpenAI: Building the compute infrastructure for the Intelligence Age

- Intel: Intel and Trump Administration reach historic agreement

- AP: US will get a 15 percent cut of Nvidia and AMD chip sales to China

- Axios: Bernie Sanders unveils AI tax plan

- AP: OpenAI and Anthropic limit new AI models during cybersecurity review

- AP: Trump administration lifts restrictions on Anthropic Claude models