Apple has spent years selling supply chain mastery as part of the product. Now the supply chain is asking a harder question: how much political risk fits inside a MacBook?

The Apple CXMT memory deal is a stress test for every builder whose hardware, cloud bill, or AI roadmap depends on memory staying boring. It is no longer boring. Apple is reportedly seeking U.S. government comfort to buy memory chips from ChangXin Memory Technologies, known as CXMT, while TrendForce says conventional DRAM contract prices are expected to rise 58 to 63 percent quarter over quarter in Q2 2026. That single number explains why a supplier choice has become a Washington story.

If you ship software, this can sound distant. It is not. RAM and NAND sit under the devices your users buy, the servers your inference stack rents, and the developer machines your team expects to last for four years. When memory gets scarce, product roadmaps start inheriting choices made in fabs, trade offices, and procurement war rooms.

What is Apple asking Washington to bless?

Apple is pressing the White House for approval to buy memory chips from CXMT, according to a June 27, 2026 report from Fortune and Bloomberg that cited the Financial Times and six people familiar with the matter. The important detail is the shape of the ask: Apple reportedly wants assurance that CXMT will not be moved into a harsher trade category after Apple builds a procurement path around it.

CXMT appears on the Pentagon’s Section 1260H list, where the Department of Defense identifies ChangXin Memory Technologies as a Chinese military company operating in the United States. That label works as a warning label rather than a direct purchase ban, which is exactly why Apple is asking for political cover instead of simply filing a normal purchase order.

The more dangerous list is Commerce’s Entity List. The Bureau of Industry and Security says the Entity List imposes license requirements and limits most license exceptions for exports, reexports, and transfers involving listed parties. If CXMT were added there, a clean commercial supplier decision could turn into a licensing problem with delay, uncertainty, and public scrutiny baked in.

That is why this story has teeth. Apple can probably find lawyers to thread the current rule set. The harder question is whether it can convince Washington that a lower memory bill is worth normalizing a relationship with a supplier the Pentagon has already flagged.

The political pushback is already loud. Representative John Moolenaar, chair of the House China committee, told the Financial Times that Apple choosing to partner with a Chinese military company would be a "grave mistake," according to Tom’s Hardware’s account of the report.

Why did memory become the expensive part of the AI stack?

The short answer is that AI infrastructure has been eating the memory market from the profitable end first. HBM, server DRAM, enterprise SSDs, high capacity RDIMMs, and storage tiers for inference are pulling capacity and management attention away from consumer devices.

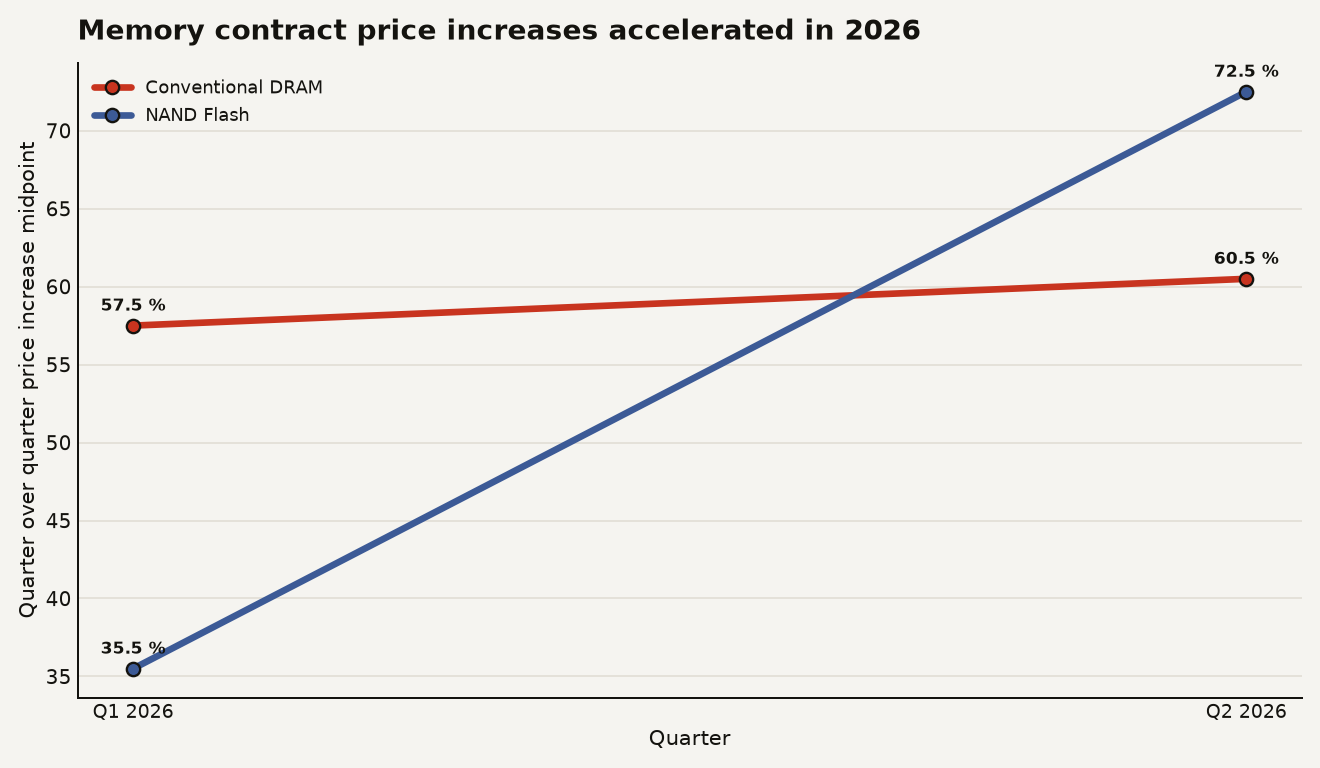

TrendForce said on March 31, 2026 that DRAM suppliers were reallocating capacity toward HBM and server applications, with conventional DRAM contract prices projected to rise 58 to 63 percent quarter over quarter in Q2 2026. The same report put NAND Flash contract price growth at 70 to 75 percent for the same quarter, driven by AI and data center demand.

This did not come out of nowhere. TrendForce said on January 5, 2026 that conventional DRAM contract prices were forecast to rise 55 to 60 percent quarter over quarter in Q1 2026, while NAND Flash prices were expected to increase 33 to 38 percent. Two quarters of that kind of movement turn memory from a procurement line item into a product strategy problem.

The chart below converts those TrendForce ranges into midpoints, so the shape is easier to see: conventional DRAM stayed near a 60 percent quarterly jump, while NAND accelerated from 35.5 percent to 72.5 percent.

Apple’s reported request sits in that squeeze. The company is not hunting for an exotic accelerator. It is looking for commodity memory capacity at a time when commodity has become a funny word. If the high margin end of the market is sold into cloud and AI infrastructure, everyone else moves down the priority list.

You can already see the pressure leaking into product pricing. Tom’s Hardware reported on June 26, 2026 that Apple raised the MacBook Air from $1,099 to $1,299, the MacBook Pro from $1,699 to $1,999, and the iPad Pro from $999 to $1,199 amid the memory crunch. That is the consumer version of the same signal: memory inflation is now large enough to move sticker prices at Apple scale.

Data Today has been tracking the same pressure from the bottom of the market, where the RAM price shock killed a budget phone before Apple’s own price moves made the story impossible to ignore. Low end hardware feels it first because there is less margin to absorb a memory spike. Premium hardware feels it later, then passes it along with better packaging and a calmer font.

Why should builders care about one Apple supplier request?

Apple’s supplier drama matters because it shows how quickly component scarcity can mutate into platform risk. Most software teams do not buy DRAM wafers, but they do make assumptions about device refresh cycles, cloud pricing, edge AI feasibility, and customer willingness to pay for local compute.

Here is the builder translation:

- Your local AI roadmap depends on device memory ceilings. If laptops and phones get more expensive, users keep old machines longer, and your on-device feature has to run on the installed base you actually have.

- Your cloud cost model depends on the same shortage. AI inference pushes demand for server DRAM and enterprise SSDs, so the memory line inside your cloud provider’s capex can show up later as instance pricing, capacity limits, or reserved commitment pressure.

- Your procurement risk now includes geopolitics. A cheap supplier can become a restricted supplier between a roadmap review and a launch window.

- Your moat gets thinner if your product only works in the high memory future. A competitor that degrades gracefully on 16GB machines may beat a fancier system that assumes 32GB is the new floor.

The Apple angle also punctures a lazy assumption about scale. Apple has one of the strongest procurement machines in the world. If Apple is asking Washington for comfort around a flagged Chinese supplier, your startup’s hardware vendor or cloud partner has less room than you think.

The software consequence is plain: build for memory variance. That means quantization, smaller local models, adaptive context windows, better caching, and user visible fallbacks that do not feel like broken promises. The engineering team that treats memory as an infinite background resource is volunteering to become a pricing casualty.

There is also a business consequence. If you sell AI features as a bundle, your gross margin can get hit twice: first by inference costs, then by the customer’s slower hardware upgrade cycle. A buyer facing a $200 laptop price increase is less patient with a SaaS vendor asking for another AI add on fee.

What should you do before the next memory bill lands?

Start by moving memory from the infrastructure footnotes into the product plan. That sounds boring, which is usually how you know it will save money.

For software and AI teams, the immediate checklist is simple:

- Profile memory per feature, not just latency. A chatbot that feels fast in a demo can become expensive when long context, retrieval, and tool traces pile up across thousands of sessions.

- Set explicit hardware floors. If your desktop app quietly assumes 32GB of RAM, say so before support tickets do it for you.

- Keep a small model path alive. A 7B or 8B class fallback can preserve a feature when the premium path is too costly or too slow.

- Negotiate cloud commitments with memory sensitivity. Ask vendors what happens if high memory instances tighten in the second half of 2026.

- Treat supplier geography as roadmap input. If a component or API depends on a politically fragile vendor, assign it the same risk weight you would assign a security dependency.

For hardware companies, the lesson is sharper. A cheaper bill of materials is useful only if it survives regulatory review, public pressure, and customer trust. Apple can absorb some reputational heat. Most brands cannot.

The next useful signal will be whether the Trump administration gives Apple the assurance it wants, refuses it, or lets the request hang. A formal green light would tell the market that cost pressure can bend blacklist politics. A refusal would tell device makers to eat the margin hit, raise prices, or redesign around less memory. Silence might be the most expensive option, because supply chains hate ambiguity almost as much as they hate shortages.

Watch Commerce more than Apple’s keynote. If CXMT moves toward the Entity List, the procurement question changes overnight. If it stays only on the 1260H list, buyers will keep asking whether the warning label is a wall or just a scarlet footnote.

The blacklist is becoming part of the BOM

The Apple CXMT memory deal is a reminder that the bill of materials now has invisible columns. One column is price. One is capacity. One is policy risk.

For years, builders optimized around compute. In 2026, memory is forcing the more humbling discipline: assume the cheap part can become the scarce part, and assume the scarce part can become political. The teams that plan for that will ship calmer products. The teams that ignore it will discover that RAM can veto a roadmap.

Sources

- Fortune and Bloomberg: Apple seeks U.S. approval to buy chips from blacklisted CXMT

- U.S. Department of Defense: Entities identified as Chinese military companies operating in the United States

- U.S. Bureau of Industry and Security: Entity List guidance

- TrendForce: AI server demand to drive memory contract price increases in 2Q26

- TrendForce: Memory makers prioritize server applications in 1Q26

- Tom’s Hardware: Apple reportedly lobbies for access to CXMT memory chips

- Tom’s Hardware: RAM crisis bites Apple as Mac and iPad prices rise