A cheap phone is supposed to be boring math. Pick a screen, pick a chip, squeeze the cameras, lock a price, ship. Nothing just showed that math breaking in public.

The RAM price shock has forced Nothing to cancel this year’s CMF phone, after co-founder Akis Evangelidis said the company could not build a successor that felt like a “genuine step forward” at a CMF price point, according to The Verge’s June 19 report. This matters because CMF is Nothing’s budget brand, and its current CMF Phone 2 Pro sells in the United States for $279 with 8GB of RAM and 256GB of storage on Nothing’s own product page.

That price class has no fat. When memory becomes the loudest line in the bill of materials, budget hardware loses its old playbook. The casualty is a phone, but the signal is bigger: AI infrastructure is now competing with consumer devices for the same memory supply chain.

What exactly did Nothing cancel?

Nothing did not announce a delayed launch date. It said there will be no new CMF phone this year.

Evangelidis wrote that CMF had been working on a successor, but “with memory prices where they are right now” the company could not build the phone at a price that made sense for the brand, as The Verge reported on June 19, 2026. That is a clean admission. The company is saying the product would either cost too much, improve too little, or both.

The existing CMF Phone 2 Pro helps explain the bind. In the U.S., Nothing lists the device at $279 with 8GB RAM, 256GB storage, a 6.77 inch AMOLED display, and a 5,000 mAh battery on the CMF Phone 2 Pro product page. A successor has to beat that spec sheet enough to feel new, while staying near a bargain price that buyers already anchor on.

Nothing CEO Carl Pei had already warned that the pressure was acute. Pei said memory was now the most expensive component in a smartphone and could account for more than 50 percent of the hardware bill, according to Lowyat’s archive of his June 12 X post. He also said memory costs for the Phone 4a doubled between product decision and launch, then doubled again after launch, in the same Lowyat-cited post.

That is the part builders should care about. The constraint hit during the product cycle, after design decisions were already locked. A team can plan around a higher component cost at kickoff. A doubling after commitment turns roadmap confidence into spreadsheet theater.

How big is the memory price move behind this?

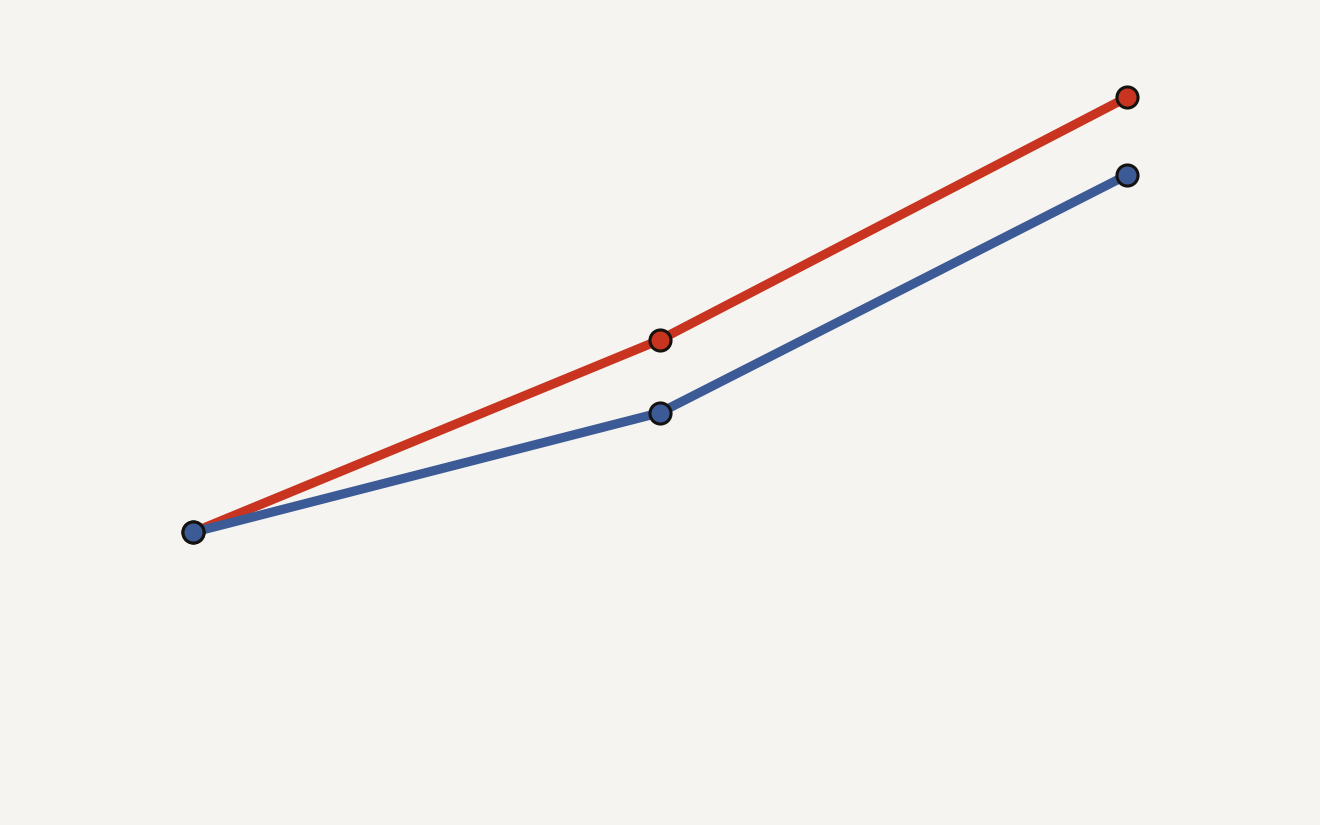

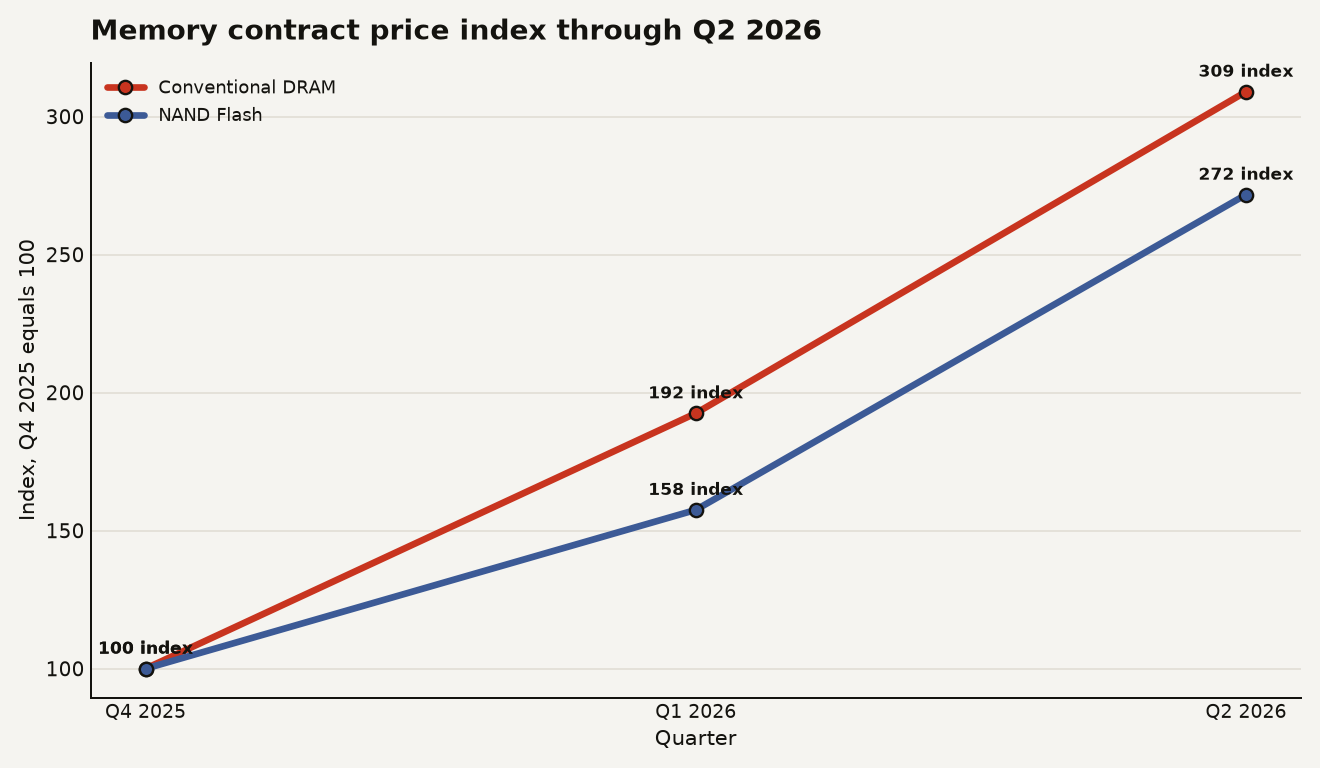

The market data backs up the pain. TrendForce raised its 1Q26 conventional DRAM contract price forecast to 90 to 95 percent quarter over quarter and its NAND Flash forecast to 55 to 60 percent quarter over quarter in a February 2, 2026 memory outlook. On March 31, TrendForce said conventional DRAM contract prices would rise another 58 to 63 percent in 2Q26, while NAND Flash would rise 70 to 75 percent, in its 2Q26 pricing survey.

Using TrendForce’s 1Q26 midpoint, a conventional DRAM index that starts at 100 in Q4 2025 reaches 192.5 in Q1 2026, based on the February forecast range. Applying TrendForce’s 2Q26 midpoint lifts the same index to 309 by Q2 2026, based on the March 31 forecast. NAND follows a similar path, from 100 to 157.5 to 271.7.

The chart below shows the compounding effect. A 60 percent jump after a 92.5 percent jump does not feel like a second headline. It feels like a new cost base.

The driver is allocation, not a sudden consumer-phone boom. TrendForce said DRAM suppliers were reallocating capacity toward HBM and server applications in 2Q26, while cloud service providers were securing supply through long-term agreements, in the same March 31 survey. Micron’s fiscal Q2 2026 release said it set records for revenue, gross margin, EPS, and free cash flow, driven by “strong demand environment” and “tight industry supply,” according to Micron’s March 18 results.

That is the ugly symmetry of the AI buildout. Data centers buy memory with enterprise budgets and strategic urgency. Budget-phone makers buy memory into a customer base that notices every $20.

Why should a developer or founder care about a missing CMF phone?

Because this is what downstream inflation looks like when AI leaves the cloud bill and enters the device bill.

If you build mobile software, you have probably spent the last two years assuming every new phone gets a little more RAM, a little more storage, and a little more local AI headroom. The CMF cancellation says the bottom of the market may move the other way. Cheaper phones can ship later, ship with smaller memory configs, or disappear for a cycle.

That changes product choices in painfully practical ways:

- On-device AI gets narrower. If a budget Android buyer stays on an older 6GB or 8GB phone for another year, your local model, vector cache, or media pipeline has less room to breathe.

- App memory discipline becomes a feature. Lazy background services, oversized SDKs, and giant startup graphs become more expensive when replacement cycles stretch.

- Cloud fallback costs rise. If local inference is less available on low-end devices, more requests route back to servers, which means the same AI infrastructure squeeze shows up twice.

- Emerging-market roadmaps get harder. CMF’s price point matters in India, Southeast Asia, and Europe’s value segment, where a $50 retail increase can erase a launch plan.

This also hits hardware founders in a familiar place: product segmentation. A budget device can usually absorb one compromise. Maybe the camera is weaker. Maybe the frame feels cheaper. Maybe storage is smaller. When the expensive part is memory, the compromise touches performance, multitasking, AI features, and longevity at once.

The same pattern is already visible beyond Nothing. Apple plans to raise product prices to offset rising memory and storage costs, and Tim Cook told The Wall Street Journal that price increases were “unavoidable,” according to Reuters coverage published June 17, 2026. Apple can pass cost into premium pricing more easily than CMF can. That contrast is the story.

The moat lesson is blunt. If your hardware business depends on aggressive retail pricing and thin margins, component access is part of your product moat now. Brand, industrial design, and software polish still matter. Supplier priority matters more when the shelves get thin.

For software companies, the safer bet is to design as if the median device improves more slowly than the flagship keynote suggests. Data Today has covered the same infrastructure pressure from the other side, where flexible data centers turn AI power into a grid dial. Memory is becoming another dial. Hyperscalers can turn it harder than a budget-phone team.

What should builders do before this spreads?

Start by treating memory as a roadmap dependency, not a background assumption.

For app teams, the practical work is unglamorous and valuable. Measure cold start memory. Audit SDKs. Put model size on the same review checklist as latency. If your “lite” app is just the main app with fewer features hidden, it will fail the users who most need it.

A useful rule for 2026 planning: design your baseline experience for last year’s budget phone, then make premium local AI additive. Nothing’s current CMF Phone 2 Pro has 8GB of RAM, and that should feel like a ceiling for mass-market assumptions rather than a floor, based on Nothing’s published spec. If your feature needs 12GB to feel good, call it a premium feature in the roadmap and price it honestly.

Hardware teams have a different set of moves:

- Lock memory supply earlier, even if it makes the product plan less flexible.

- Build SKUs around fewer memory configurations so procurement has more volume per part.

- Spend engineering time on compression, caching, and storage tiering before adding another sensor.

- Avoid promising device AI features that require a future memory price collapse.

The last point deserves emphasis. AI marketing wants local models everywhere. The supply chain is saying: prove the unit economics first.

There is also a business communication lesson in Nothing’s move. Canceling a phone sounds embarrassing, but shipping a weak successor at a bad price would damage the brand more. CMF’s promise is value. If the company cannot defend that promise in 2026, skipping the cycle is cleaner than teaching customers to distrust the badge.

Could the RAM price shock ease before 2027 phones ship?

It could, but the evidence points to tight supply lasting through the next planning cycle.

TrendForce tied the 2Q26 increase to AI server demand, HBM capacity shifts, and cloud providers using long-term agreements to secure supply in its March 31 pricing note. Those are slower-moving forces than holiday phone demand. A retailer can discount old inventory in November. A memory supplier cannot instantly turn HBM-oriented capacity back into cheap mobile DRAM without giving up better customers.

Micron’s financials also show why suppliers have little reason to rush back to bargain pricing. The company reported $13.6 billion in fiscal Q2 2026 revenue and guided for $16.2 billion in fiscal Q3 revenue at the midpoint in its March 18 earnings release. When tight supply produces record results, procurement teams should expect tough negotiations.

The open question is demand elasticity. If consumer electronics buyers reject higher phone, PC, and console prices, device makers may cut specs or delay launches. If AI infrastructure spending slows, memory pressure can cool. Neither outcome helps a 2026 budget phone that needed parts ordered months ago.

For builders, the forward read is simple enough: assume memory remains expensive through your next release cycle. Optimize now. Price now. Cut the feature that only works on a fantasy bill of materials.

Cheap phones are where AI’s bill becomes visible

The AI boom usually arrives as a cloud invoice, a power constraint, or a GPU waitlist. Nothing’s canceled CMF phone gives it a retail price tag.

A missing $279 phone will not slow the data center race. It will remind everyone else that the race has a cover charge.

Sources

- The Verge: Nothing cancels this year’s CMF phone due to RAM prices

- Nothing: CMF Phone 2 Pro product page

- Lowyat.NET: Carl Pei says phone prices will continue to rise

- TrendForce: Memory price outlook for 1Q26 sharply upgraded

- TrendForce: AI server demand to drive memory contract price increases in 2Q26

- Micron: Fiscal Q2 2026 results

- Reuters via Investing.com: Apple to raise prices due to memory chip shortage