Palantir sells about $4.5 billion of software a year and the market values it near $400 billion. That gap is the whole story, and it is worth understanding before you decide whether the company is a generational data platform or the most expensive ticker on the S&P 500.

Palantir Technologies was founded in 2003 by Peter Thiel, Alex Karp, Stephen Cohen, Joe Lonsdale and Nathan Gettings, and named after the seeing stones in Tolkien. For most of its life it was a secretive contractor that helped spy agencies and soldiers make sense of messy data, and it lost money for roughly twenty years. Then two things happened at once: it turned its first GAAP profit in early 2023, and a few months later it shipped an AI product at the exact moment every enterprise on earth started asking what to do with large language models. The result is a stock that trades at roughly 90 times sales, a multiple normally reserved for pre-revenue startups, not 23-year-old government suppliers.

What does Palantir's software actually do?

Strip away the mystique and Palantir solves a boring, expensive problem: big organizations cannot find or trust their own data. Their records sit in dozens of incompatible systems that were never meant to talk to each other. Palantir's platforms pull those records into a single working model, then let analysts, and now AI agents, act on it.

There are four platforms, and they map cleanly onto who buys them.

| Platform | Launched | What it does | Who runs it |

|---|---|---|---|

| Gotham | 2008 | Fuses intelligence and battlefield data for investigations and targeting | US defense and intelligence, Ukraine's military, police forces |

| Foundry | 2016 | Builds a live data model of a whole business or agency | Airbus, Ferrari, Merck KGaA, NHS England |

| Apollo | 2021 | Continuously ships and updates the software into secure environments | Internal delivery layer for every Palantir deployment |

| AIP | 2023 | Plugs LLMs into private data so agents can read and act inside it | Enterprises adopting AI, plus government users |

The piece that ties it together, and the part you should actually copy, is the ontology. Instead of pointing an AI model at a pile of raw tables, Palantir builds a digital twin of the business: the customers, the trucks, the orders, the machines, and the rules that connect them. AIP's agents reason over that model rather than over the underlying database mess. Wired once described the company as a technical band-aid that lets customers integrate and analyze data without fixing their broken architecture first, and that is meant as praise, not an insult. Notably, Palantir does not collect or store the data itself. Customers bring their own records and keep the rights to them, which is why a defense ministry and a carmaker can both run it.

The other half of the product is human. Palantir embeds its own staff, called forward deployed engineers, directly inside a customer to wire the system up, and runs five-day boot camps to get teams building. It is a services-heavy way to sell software, and it is the reason pilots so often turn into seven-figure expansions.

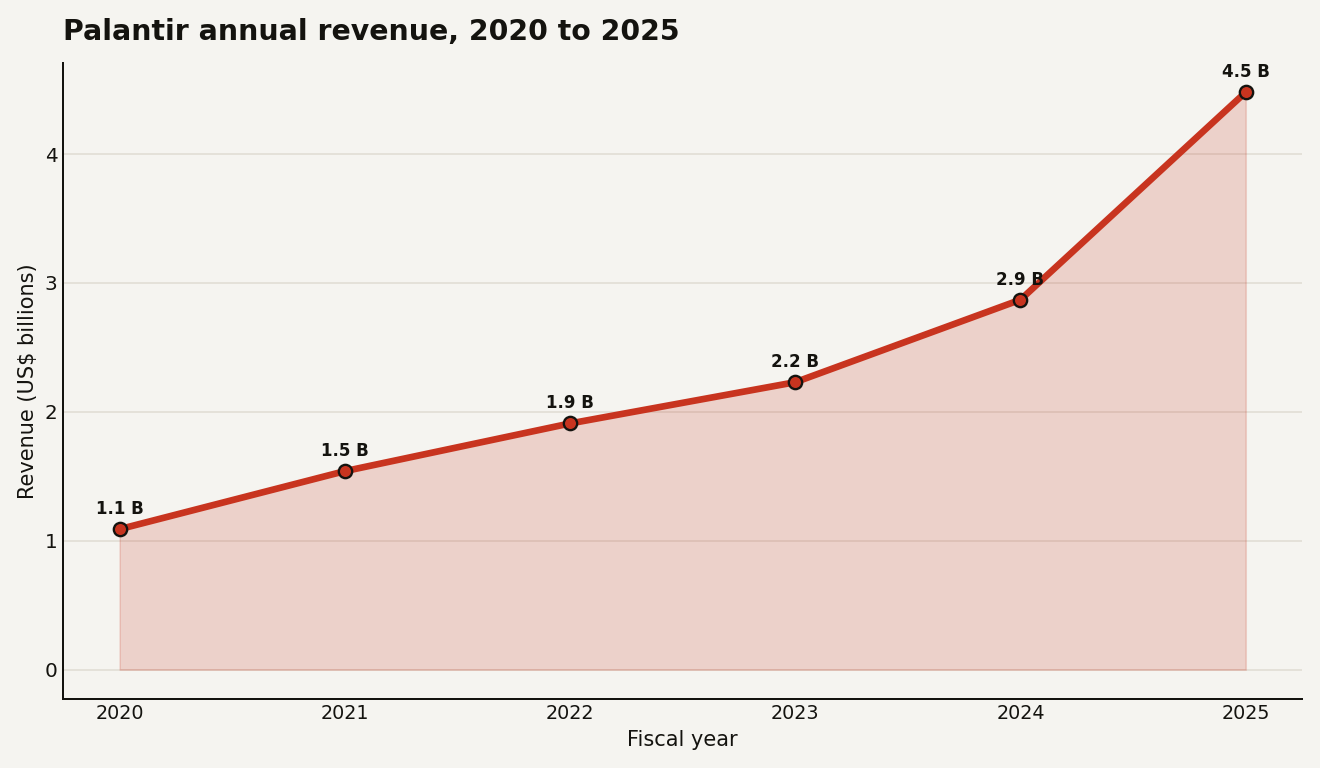

How fast is the money actually growing?

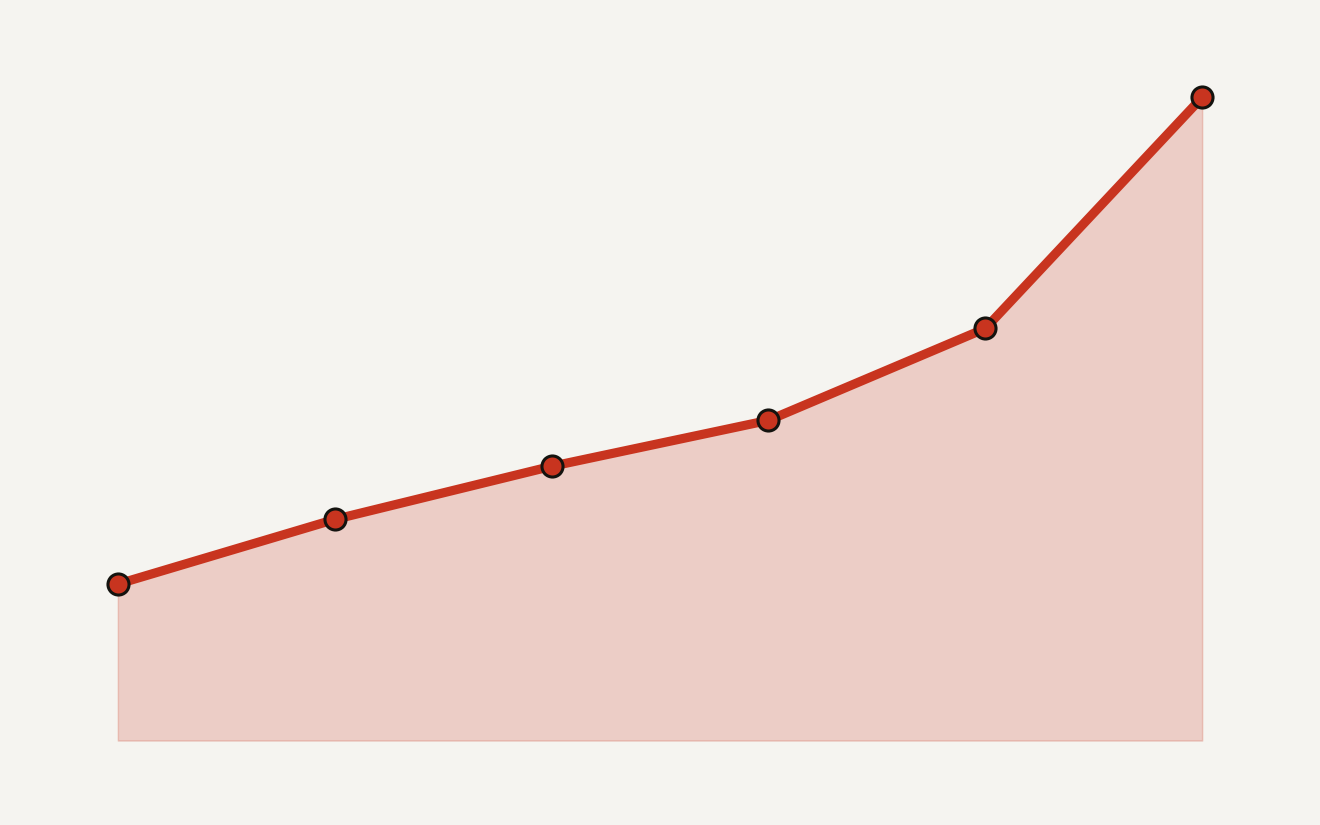

The growth is real and it is accelerating, which is the part bears underrate. Revenue went from $1.09 billion in 2020 to $4.48 billion in 2025, and the curve is steepening rather than flattening.

The 2025 numbers carry the bull case. Full-year revenue rose about 56 percent over 2024, and the company reported net income of $1.63 billion, a clean profit rather than an adjusted one. The standout line was US commercial: in the fourth quarter that segment grew 137 percent year over year to $507 million, the signal that AIP is selling to companies and not just to generals. Total revenue still splits close to evenly, about 54 percent government and 46 percent commercial, but the commercial side is where the acceleration lives.

The government side is not standing still either. In July 2025 the US Army consolidated 75 separate contracts into a single enterprise agreement with Palantir worth up to $10 billion over ten years, the kind of deal that turns a vendor into infrastructure. Once an agency runs its operations on your ontology, switching costs become close to prohibitive, which is exactly what a high multiple is supposed to be paying for.

So why is it worth nearly 90 times sales?

Here is where discipline matters, because the valuation is genuinely extreme. The Economist called Palantir possibly the most over-valued firm of all time in August 2025, pegging its market value around $430 billion, more than 600 times its 2024 earnings. By late 2025 it was the most expensive stock in the S&P 500 at about 85 times expected forward sales. For context, a strong enterprise software company usually trades in the teens on that measure. Palantir's headcount is only around 4,400 people, too small to clear the revenue bar for the Fortune 500, yet the company sits among the 25 most valuable in the world.

So what is the market actually paying for? Three things, in order of how defensible they are:

- The integration layer for AI. Agents are only as good as the data they can reach. Palantir sells the plumbing that makes enterprise data legible to a model, and that plumbing gets stickier every quarter a customer relies on it.

- Government lock-in. Mission-critical defense and intelligence work is slow to win and almost impossible to displace. The $10 billion Army deal is a moat priced as a growth story.

- A bet on flawless execution. This is the fragile part. At 85 times sales the stock needs years of 40-percent-plus growth with fat margins and almost no stumbles. Any miss gets punished hard.

The honest read is that the data technology justifies a premium and the share price justifies skepticism. The ontology and the forward deployed model are a real, durable advantage. A multiple in the high double digits is not a valuation, it is a prediction, and the prediction is that Palantir becomes the default operating system for serious institutions. That can come true and the stock can still be too expensive today.

What should you take from this if you build with AI?

You do not need to own the stock to learn from the product. The most useful idea in Palantir's whole business is that the bottleneck for enterprise AI is not the model, it is the data model underneath it. That lesson generalizes far beyond one vendor.

- If you are shipping agents, invest in a clean semantic layer before you invest in a bigger model. An agent reasoning over a coherent ontology beats a smarter agent guessing at raw tables. This is the same fight covered in the debate over who cleans the data.

- If you are buying, separate the software from the services. A lot of Palantir's value is delivered by humans on site. Price the boot camps and the engineers into your total cost, not just the license.

- If you are building a competitor, the opening is the price, not the product. Plenty of teams can integrate data; few have a decade of government trust and a self-reinforcing install base.

The caveats are real and worth saying out loud. Revenue is concentrated in the US, with about 74 percent of sales coming from American customers, so a domestic budget shift hits hard. The founders keep near-permanent control through a special class of shares that locks in close to half the vote regardless of dilution, so public shareholders are along for the ride, not steering. And the politics are not neutral: Palantir's work with immigration enforcement and on the battlefield is a reputational variable that a pure software story tends to ignore.

Palantir built something genuinely hard: a way to make an institution's data usable by machines without first rebuilding the institution. That is worth a lot. Whether it is worth $400 billion depends entirely on a future that has not happened yet, and you are allowed to admire the engineering while doubting the price.

Sources

- Palantir Technologies 2025 annual report and SEC 10-K filing

- Palantir investor relations and quarterly results

- The Economist, "Is Palantir the most over-valued firm of all time?"

- Wired, "What Does Palantir Actually Do?"

- US Army announcement of the Palantir enterprise agreement

- Fortune coverage of Palantir's market value