Oracle has given the AI labor story a more useful shape than the usual robot-takes-job headline. The Oracle AI layoffs were not only a productivity story. They were a capital allocation story, with 21,000 fewer full-time employees sitting beside a debt-funded race to build AI cloud capacity.

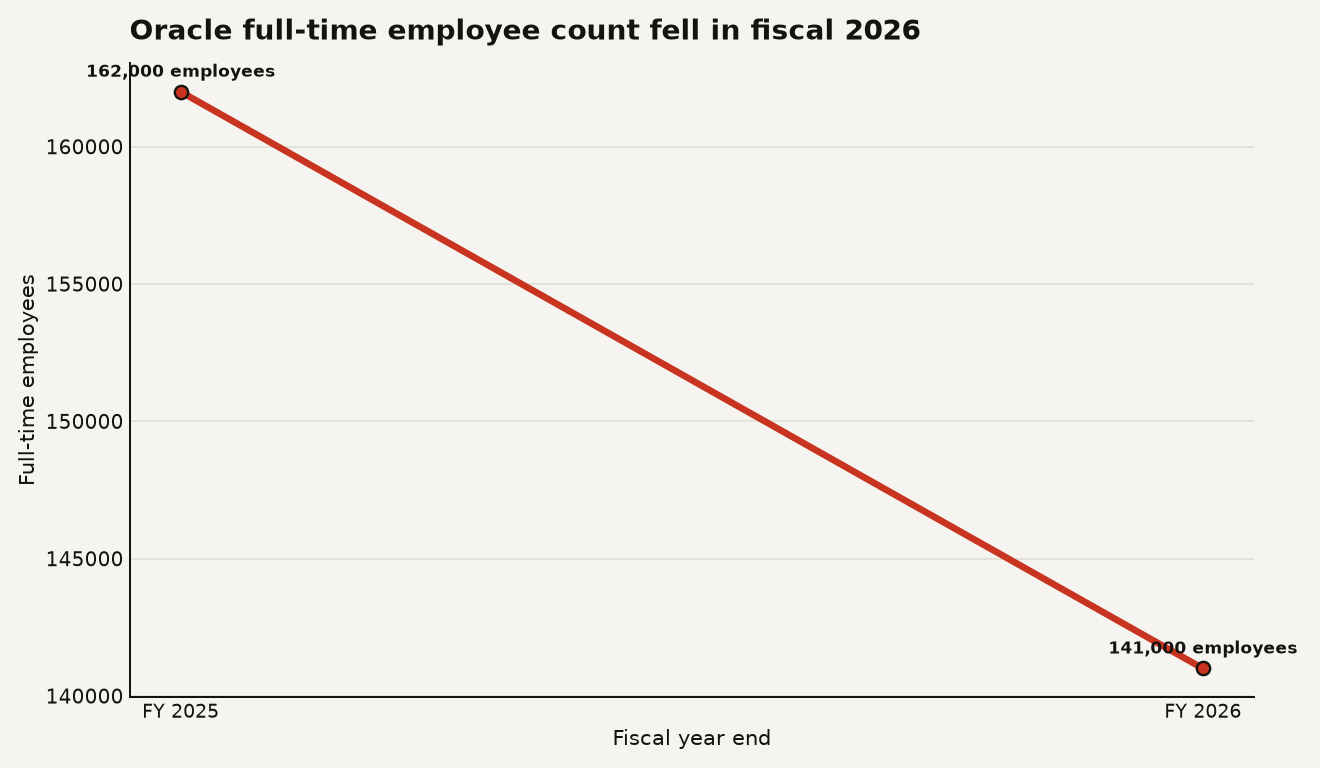

Here is the blunt version. Oracle ended fiscal 2026 with 141,000 full-time employees, down from 162,000 a year earlier, according to its 2026 Form 10-K and its 2025 Form 10-K. In the same fiscal year, Oracle said it raised $43 billion in debt financing and $5 billion in equity financing, according to its June 10, 2026 earnings release.

That pairing matters if you build on Oracle, compete with Oracle, sell into the CIO office, or run a company trying to copy the AI playbook. The new enterprise AI bargain is not simply better tooling for fewer people. It is fewer people, more GPUs, more financing risk, and a much tighter question about which parts of the business deserve human payroll.

What did Oracle actually disclose about the cuts?

Oracle did not announce a single clean layoff number in a standalone press release. The number comes from two annual filings.

Oracle reported approximately 141,000 full-time employees as of May 31, 2026 in its latest annual report. Oracle reported approximately 162,000 full-time employees as of May 31, 2025 in its prior annual report.

That is a net reduction of 21,000 people, or about 13 percent of the prior year headcount. The chart shows the simple part of the story: the workforce line moved down hard in one fiscal year.

The harder part is why. In its fiscal 2026 risk language, Oracle said the adoption and deployment of AI technologies across its operations have resulted, and may continue to result, in workforce reductions, according to the 2026 Form 10-K. The filing also tied its restructuring plan to a continued emphasis on developing, marketing, selling, and delivering cloud-based offerings.

Oracle’s restructuring bill got large at the same time. The company recorded $1.8 billion of restructuring expenses in fiscal 2026, up from $374 million in fiscal 2025, according to the same 2026 annual filing. That is the number to watch if you are tempted to treat AI layoffs as instant margin magic.

Severance has a cash cost. Lost internal knowledge has a product cost. Slower support has a customer cost. Oracle even warned about reduced productivity, shortages of sufficiently skilled employees in certain roles, loss of institutional knowledge, and damage to morale and retention in its 2026 Form 10-K.

The filing reads like an executive committee trying to do two things at once: make the cost base fit the AI cloud buildout, then warn investors that the surgery can leave scar tissue.

Why is this tied to Oracle’s AI cloud bet?

Oracle’s AI infrastructure push is measured in finance numbers, not vibes.

Oracle said on February 1, 2026 that it expected to raise $45 billion to $50 billion of gross cash proceeds during calendar 2026 to build additional capacity for large Oracle Cloud Infrastructure customers, including AMD, Meta, NVIDIA, OpenAI, TikTok, and xAI, according to its financing plan announcement. Then, in June, Oracle said it had raised $43 billion in debt financing and $5 billion in equity financing during fiscal 2026, according to its FY 2026 earnings release.

That same earnings release said Oracle’s remaining performance obligations reached $638 billion at the end of Q4, up $85 billion sequentially from Q3. Oracle also said the prepaid and customer supplied hardware portions of large AI contracts totaled $75 billion, a structure the company said reduces how much capital it must raise to build AI data centers.

This is the tension. Oracle has demand signals that most cloud vendors would love to put on a slide. It also has a bill for capacity that arrives before the most profitable parts of those contracts fully show up in revenue.

The labor cuts help the cash model. If a company needs tens of billions for data centers, GPUs, networking, power, and lease commitments, payroll becomes one of the few large operating lines that management can move within quarters rather than years.

That does not mean every eliminated role was replaced by a model. It means AI can hit employment through at least three channels:

- Direct substitution, where a workflow needs fewer people because software handles more of the work.

- Capital reallocation, where headcount is cut to fund GPUs, data centers, power commitments, and debt service.

- Org redesign, where cloud and AI teams receive resources while legacy, support, sales, or back-office groups lose them.

Oracle’s disclosure points to all three, but the second channel is the under-discussed one. The market keeps asking whether AI can write the code. Oracle is showing that AI can also rewrite the budget.

Why should builders care if they never touch Oracle stock?

Because your roadmap may depend on a vendor that is making the same trade.

If you buy infrastructure from Oracle Cloud Infrastructure, the good news is obvious. Oracle is chasing scale, and its reported cloud infrastructure revenue rose 77 percent in fiscal 2026 to $18.1 billion, according to its June 2026 earnings release. More capacity can mean better access to GPUs, more aggressive enterprise pricing, and stronger options for teams that want a hyperscaler alternative.

The risk is operational. A 13 percent net headcount reduction at a company with deeply embedded enterprise software can show up as longer support loops, thinner account coverage, slower migrations, and more brittle institutional knowledge. If your finance, healthcare, database, or cloud estate depends on Oracle, your risk review should include people capacity, not only service-level agreements.

There is also a competitive signal here. Oracle’s move says the AI infrastructure race rewards companies that can finance the bridge between promised demand and delivered capacity. That is a very different moat from having a clever model wrapper or a shiny agent demo. It is closer to project finance with an API.

For builders, the practical consequences are sharper than the macro debate:

- Your cloud bill may become a financing pass-through. If providers fund huge AI capacity with debt and equity, pricing pressure will eventually reflect the cost of capital.

- Your vendor risk model needs a people layer. A provider can expand GPU capacity while weakening the humans who help you migrate, debug, and recover.

- Your own AI savings claims need a cash timeline. Oracle spent $1.8 billion on restructuring in fiscal 2026, so any board slide promising instant savings should account for transition cost.

- Your moat should avoid pure capacity dependency. If your product advantage rests only on access to scarce compute, a larger balance sheet can copy that advantage faster than you think.

This is why Data Today has been watching the physical AI stack as closely as the model layer. The same pressure shows up in AI power and grid planning, where data centers become flexible loads rather than ordinary office buildings.

Is Oracle an outlier, or part of a broader AI layoff pattern?

Oracle is large enough to matter on its own, but it also fits a broader shift in how companies explain job cuts.

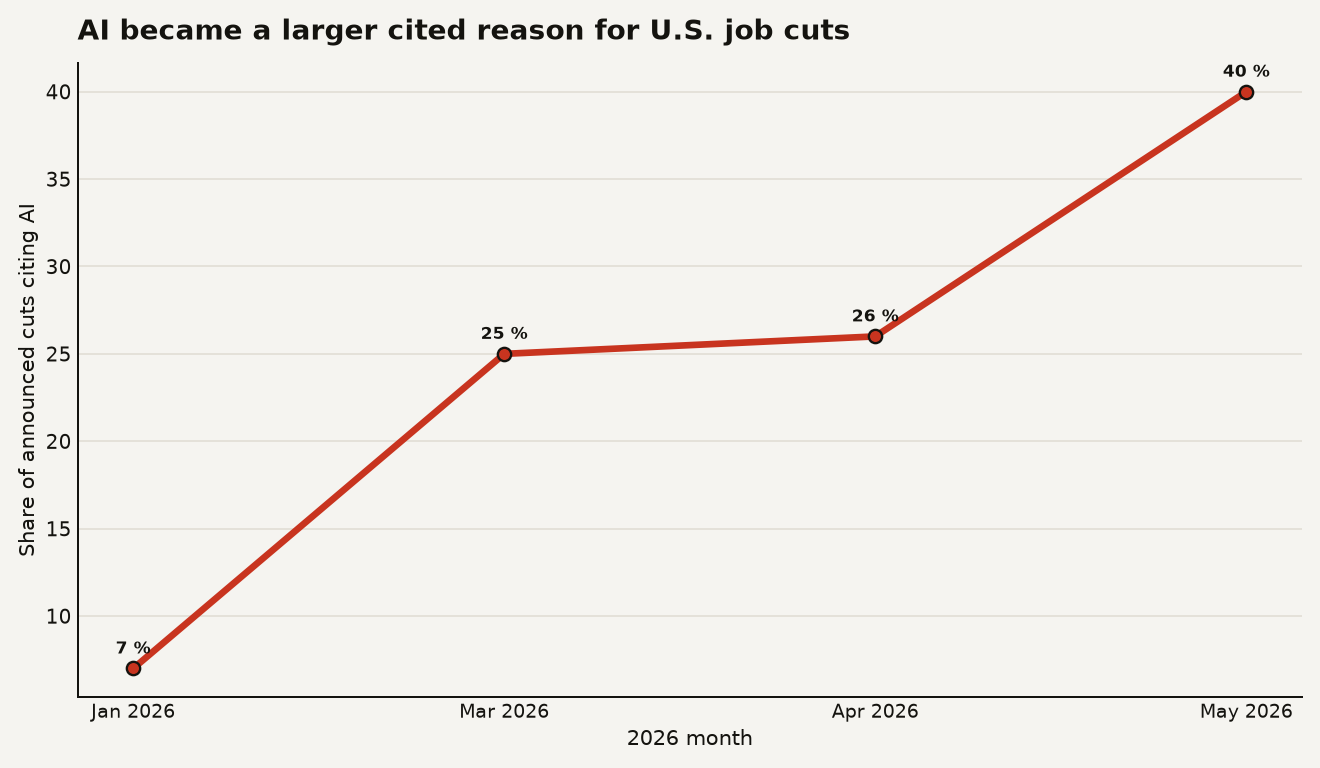

Challenger, Gray and Christmas said U.S. employers announced 97,006 job cuts in May 2026, and the firm said AI was cited for 38,579 of those cuts, or 40 percent of the month’s total, in its May 2026 job cuts report. The same report said AI had been cited in 87,714 cuts so far in 2026, already above the 54,836 attributed to AI in all of 2025.

The monthly share is moving fast, as the chart shows. Challenger reported AI at 7 percent of announced cuts in January 2026, 25 percent in March, 26 percent in April, and 40 percent in May.

There is a trap in those numbers. “AI cited” does not prove “AI did the job.” Companies use AI as a reason, a strategy label, a budget shield, and sometimes a convenient story for cuts they wanted to make anyway.

Still, the label changes behavior. When executives can tell boards that workforce reductions fund AI capacity or AI transformation, cuts that once looked defensive can be repackaged as investment. That makes it easier for a company to reduce headcount while telling investors it is leaning into growth.

Oracle’s case is cleaner than most because the filings connect the dots: fewer employees, explicit AI adoption language, a cloud restructuring plan, a big restructuring charge, and a massive AI infrastructure financing program.

What should you do if Oracle sits in your stack?

Treat this as a dependency audit, not a panic button.

Start with the systems where Oracle is hardest to replace: databases, ERP, healthcare applications, billing, identity integrations, reporting pipelines, and OCI workloads tied to GPU availability. For each one, write down the human dependency as clearly as the technical dependency.

Ask three questions before the next renewal:

- Who supports the system now? Get named escalation paths, not only generic support tiers.

- What changed in the account team since January 2026? A vendor reorg can turn a stable implementation into a scavenger hunt.

- What is your exit path if capacity, support, or price changes? Even a partial migration plan gives you leverage.

For AI builders choosing cloud capacity, the lesson is more strategic. Oracle may be a strong option when capacity and price line up, especially for GPU-heavy workloads. But the financing intensity behind the buildout means you should avoid designing a system that assumes one provider’s economics stay friendly forever.

Use portability where it matters: containerized serving, clean data export paths, model abstraction that does not hide every provider-specific cost, and contracts that preserve your ability to shift inference or training jobs. You do not need perfect multicloud purity. You need enough optionality that a pricing email does not become a roadmap meeting.

For founders, the hiring lesson is uncomfortable. If your AI plan depends on cutting support, customer success, or implementation roles, you may save cash while weakening the exact trust layer that enterprise buyers pay for. Oracle can absorb more turbulence than a 60-person startup. You probably cannot.

What should you watch next?

Watch the backlog conversion, the support quality, and the debt story.

Oracle guided to $90 billion of total revenue for fiscal 2027 in its June 2026 earnings release. That number matters because the company’s AI cloud thesis needs bookings to become revenue, revenue to become cash, and cash to justify the financing load.

Watch the legal and credit side too. A January 2026 complaint in New York alleged Oracle issued $18 billion of senior notes in September 2025 and later needed an additional $38 billion of debt sales for AI infrastructure, according to the bondholder complaint. Those are allegations, not court findings, but they show where investor anxiety lives: disclosure, leverage, and dependence on huge AI infrastructure contracts.

The worker story will also keep moving. Challenger said technology companies announced 123,653 job cuts through May 2026, up 66 percent from the same period in 2025, in its May 2026 report. If AI remains the top cited reason for cuts through the second half of 2026, hiring plans and salary bands in enterprise software will start to reflect that new baseline.

The useful bet is not that Oracle is doomed or destined. The useful bet is that AI infrastructure has become a balance sheet business. Builders who understand that will negotiate better contracts, design more portable systems, and avoid confusing a vendor’s backlog with their own stability.

The new AI budget has a body count and a bond coupon

Oracle’s filings turn the AI boom from a keynote into a spreadsheet. The spreadsheet has GPUs on one side, employees on another, and lenders underneath both.

That is the part to remember. When AI becomes infrastructure, the tradeoffs stop looking like software margins and start looking like industrial finance. The model may answer instantly. The bill arrives on a schedule.