The AI stack has a new bottleneck, and it does not look like a GPU. It looks like a substation, a transformer order, a transmission study, and a regulator deciding who pays when a 500 MW campus wants to plug in.

Large-load interconnection moved from trade-group headache to national AI infrastructure policy on June 18, 2026, when the Federal Energy Regulatory Commission ordered six regional grid operators to justify or reform how they connect data centers, factories, and other large power users to the transmission grid. FERC said those operators have 60 days to defend their existing tariffs or propose changes, with a separate 30-day report on whether enough generation will exist to serve new and existing large loads.

That is the right frame for builders. Power is becoming an API with terrible documentation, local rate politics, and queue times that can outrun your model roadmap. If your product depends on guaranteed inference capacity in 2027, the question is no longer only which accelerator you can buy. It is whether your compute supplier can prove it is a good grid citizen.

What did FERC actually order on June 18?

FERC did not hand data centers a universal express lane. It opened a pressure campaign.

The commission issued show cause orders under Section 206 of the Federal Power Act to PJM, MISO, SPP, CAISO, ISO New England, and NYISO, requiring each grid operator and its transmission owners to explain why current rules remain just and reasonable or file tariff revisions. FERC’s fact sheet names five reform categories: faster transmission service applications and studies, cost-shift prevention, co-location and behind-the-meter generation, new transmission services for flexible large loads, and processes for studying nearby generation that serves those loads.

The key number is the clock. FERC gave the six grid operators 60 days to respond on tariffs, and it required a 30-day informational report on resource adequacy, meaning how each region expects to have enough generation to serve both current customers and new large loads. The June 18 release also says staff reviewed more than 3,500 pages of public comments before the action.

This is a regulator telling regional markets to stop treating a 1 GW data center campus like a weird one-off request. The old queue logic was built around power plants asking to inject electricity and customers growing slowly. AI broke that rhythm. A hyperscale campus can show up with demand that resembles a small city, and it wants service on a product cycle, not a utility planning cycle.

The action also draws a line around federal and state power. FERC says the orders do not intrude on state authority to site and permit generation or set retail electricity rates, while the commission is trying to prevent cost shifting among transmission customers. The FERC fact sheet puts that boundary in plain terms: federal tariffs can be pushed toward transparency, but state commissions still decide retail allocation.

NVIDIA welcomed the order for obvious reasons. The company’s June 18 post argues that large customers should fund network upgrades, bring new generation, and offer flexible load, while NVIDIA and Emerald AI are developing AI factories that can respond to grid conditions. NVIDIA said commercial deployment of that flexible AI factory work begins later in 2026.

The bullish version is attractive: data centers pay for upgrades, add generation, curtail when the grid is tight, and spread fixed grid costs across more consumption. The hard version is the one that matters: every one of those verbs needs a contract, a tariff, telemetry, enforcement, and a penalty if the campus behaves badly during a peak event.

Why is AI power demand forcing this fight now?

The demand curve stopped being theoretical.

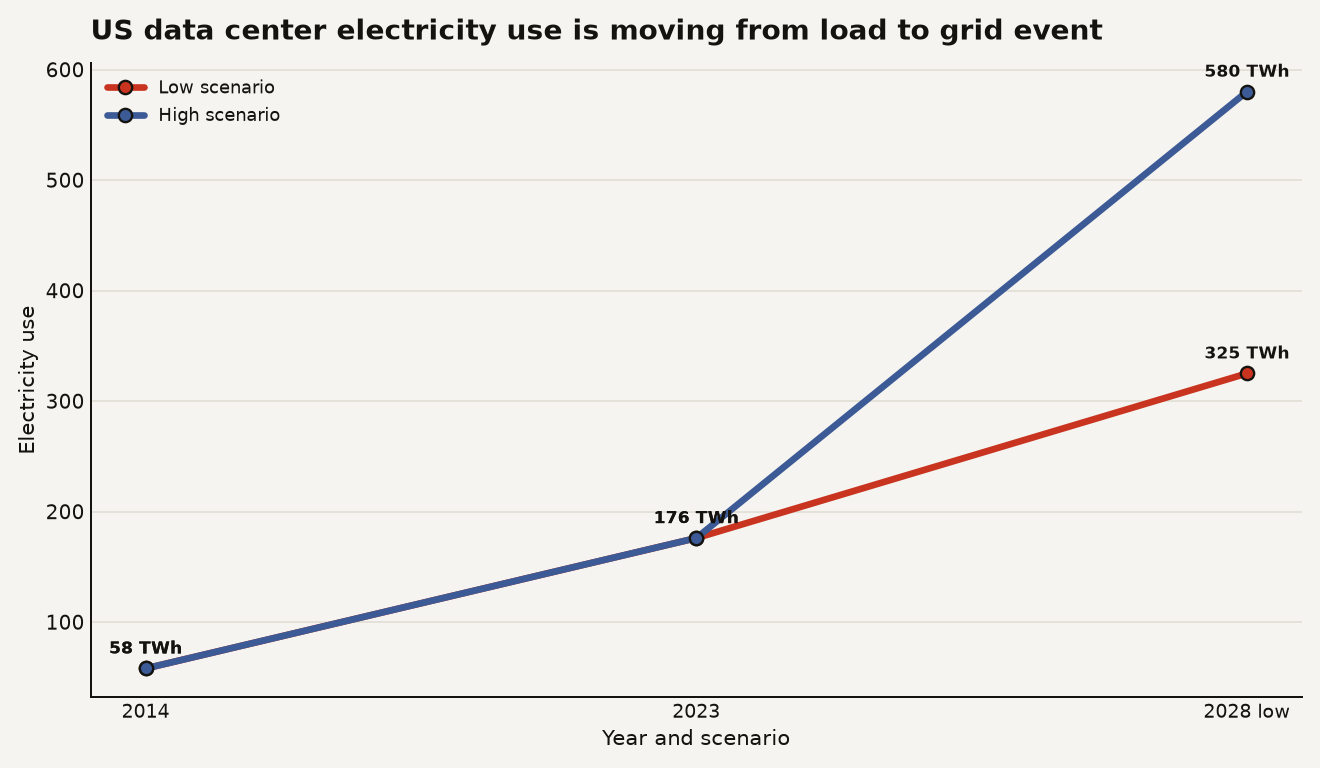

Lawrence Berkeley National Laboratory estimated that US data centers used 176 TWh of electricity in 2023, up from 58 TWh in 2014, and projected a 2028 range of 325 TWh to 580 TWh in its congressionally requested 2024 report. Berkeley Lab describes the work as a historical estimate back to 2014 with future scenarios through 2028 based on recent trends.

The chart below puts the interconnection fight in context: even the low 2028 scenario nearly doubles 2023 data center electricity use, while the high scenario more than triples it.

The International Energy Agency gives the global version of the same squeeze. Data centers consumed about 415 TWh globally in 2024, and the IEA projects that number to more than double to about 945 TWh by 2030. The IEA’s Energy and AI report says the United States accounted for 45 percent of global data center electricity consumption in 2024 and that US data centers account for nearly half of domestic electricity demand growth through 2030.

That does not mean every data center should be treated as a villain in a rate case. PG&E has been making the opposite argument in California. PG&E said in February 2025 that it was working to serve about 5.5 GW of new data center demand over the next decade and estimated that each 1 GW of new data center load could reduce customer bills by 1 percent to 2 percent over the long term.

That PG&E math rests on a condition builders should underline: new load has to use existing infrastructure better, pay its share of upgrades, and avoid making the system buy expensive capacity for a few peak hours. If a campus adds 24-hour demand in a place with spare wires and firm generation, it can lower unit costs. If it lands in a constrained pocket and forces a gas peaker, transformer rush order, and transmission rebuild, the affordability story collapses.

EIA’s near-term forecast shows why the timing is tense. The agency projected US residential electricity prices at 18.2 cents per kWh in 2026 and 18.6 cents per kWh in 2027, while US electricity generation rises from 4,509 billion kWh in 2026 to 4,639 billion kWh in 2027. EIA’s June 2026 Short-Term Energy Outlook also projects US solar capacity rising from 182 GW in 2026 to 221 GW in 2027.

A faster interconnection process can help only if supply, wires, and flexibility move together. Otherwise, FERC can shorten the paperwork while the physics keeps its calendar.

What changes for your roadmap if compute becomes a grid product?

If you buy cloud GPUs by the hour, FERC can feel distant. It is not. Large-load interconnection is about the upstream constraint on your inference margin, capacity reservations, and launch geography.

A model company that needs guaranteed serving capacity in 2027 is now exposed to utility execution risk. A SaaS company promising agentic workflows with predictable latency is exposed to data center siting risk. A startup training domain models on reserved clusters is exposed to the question nobody wants in the board deck: will the cluster have power when the contract says it will?

This is where flexible data centers as a grid dial stop being a nice sustainability slide and become a procurement requirement. Flexibility means a campus can reduce draw, shift workloads, or draw from storage and on-site generation when the grid is tight. For AI, that maps cleanly to workload classes: batch training can move more easily than real-time inference, checkpointing can absorb pauses better than interactive agents, and cold storage can tolerate scheduling games that a customer-facing copilot cannot.

What this means for you:

- Cloud procurement needs an energy appendix. Ask whether the capacity you are buying sits behind flexible load agreements, behind-the-meter generation, or a normal utility queue position.

- Architecture needs workload triage. Label jobs by interruptibility, latency sensitivity, and geographic mobility before the power market labels them for you.

- Cost models need local power risk. A cheap GPU hour in a constrained region can become expensive if curtailment, demand charges, or capacity scarcity hit the provider.

- Moats will include power operations. The best AI infrastructure companies will optimize chips, networking, cooling, and grid participation as one system.

There is also a hiring implication. Teams that run serious AI infrastructure need people who understand energy markets well enough to read a tariff and spot a cost-shift fight. That does not mean every AI startup needs a utility lawyer on staff. It does mean your infra lead should know the difference between renewable procurement, firm capacity, interconnection approval, and actual deliverable power at the node.

The unpleasant part: flexibility has a product cost. The IEA notes that an AI-focused data center can be 10 times more capital-intensive than an aluminum smelter, which makes curtailing compute expensive even when it helps the grid. The IEA report also estimates that around 20 percent of planned data center projects could face delay risks unless grid constraints are addressed.

That is the trade. The grid wants interruptibility. AI wants utilization. The winners will price the interruptibility honestly instead of hiding it in vague green-cloud language.

What should builders watch before the 60-day clock runs out?

Watch the tariff details, not the victory laps.

The first thing to watch is who pays for upgrades and when refunds apply. DOE’s October 23, 2025 directive asked FERC to consider whether large loads and co-located facilities should pay the full cost of needed grid upgrades and whether those costs should be credited back over time. FERC’s RM26-4 docket page says the DOE proposal defined large loads generally as demand greater than 20 MW and asked whether flexible loads could receive faster studies, potentially within 60 days.

The second thing to watch is measurement. A flexible data center is useful only if the grid operator can see and trust the response. That means telemetry, baselines, dispatch rules, and penalties. If the tariff lets a campus claim flexibility without proving performance during the 20 hottest hours of the year, consumers will pay for a fiction.

The third thing to watch is co-location. A data center next to a power plant can reduce transmission stress, but it can also create fights over whether existing customers lose access to a resource that used to serve the broader grid. FERC’s June 18 order flags co-location and behind-the-meter generation as one of the five reform categories, which is where many of the nastiest legal and reliability questions will sit.

The fourth thing to watch is regional divergence. SPP already has a High Impact Large Load framework, PJM has been wrestling with co-located load, and CAISO has different transmission service mechanics. FERC’s fact sheet explicitly says the orders leave room for each RTO and ISO to define large loads and set operational requirements for its region.

For an AI builder, the practical checklist is short:

- Prefer providers that disclose power availability by region, not only GPU inventory.

- Treat training jobs as movable by default unless data residency or latency blocks you.

- Negotiate service terms that distinguish compute shortage from grid curtailment.

- Track the six FERC responses before making long-term regional commitments.

A clean 60-day response from a grid operator will not magically energize a new campus. It will tell you which regions are building a rulebook for AI load and which are still negotiating with the future by email.

The grid is part of the stack now

FERC’s move is useful because it forces a more adult conversation. AI infrastructure cannot keep asking for city-scale power while pretending the grid is a passive input. Utilities cannot hide behind legacy queues while demand changes faster than their study process.

The builder move is to stop treating energy as somebody else’s procurement problem. Your model may run in a container, but your business runs on wires. The companies that understand both will ship when the rest are waiting for an interconnection study.

Sources

- Federal Energy Regulatory Commission: FERC Launches Aggressive Targeted Action to Speed Large Load Integration

- Federal Energy Regulatory Commission: Fact Sheet on Large Load Integration Orders

- Federal Energy Regulatory Commission: RM26-4 Large Load Interconnection Docket

- Lawrence Berkeley National Laboratory: 2024 United States Data Center Energy Usage Report

- International Energy Agency: Energy and AI Executive Summary

- U.S. Energy Information Administration: Short-Term Energy Outlook, Electricity, Coal and Renewables

- PG&E: Accelerating Connection of New Data Centers

- NVIDIA Blog: How FERC’s Large-Load Interconnection Actions Help Address Grid Stress