The constraint on frontier AI is no longer ideas. It is electricity and capital. Frontier labs have collectively raised more than 170 billion dollars, and a single data center with one gigawatt of facility power now costs roughly 30 billion dollars to build, according to Epoch AI. The model is the cheap part.

The buildout is visible in physical infrastructure. The largest known AI data center, the Anthropic and Amazon site at New Carlisle, draws an estimated 1.1 gigawatts and carries about 35 billion dollars in capital cost. Microsoft's planned Fairwater Wisconsin facility is projected to be nearly eight times more powerful, equivalent to 5.2 million H100 chips by September 2027.

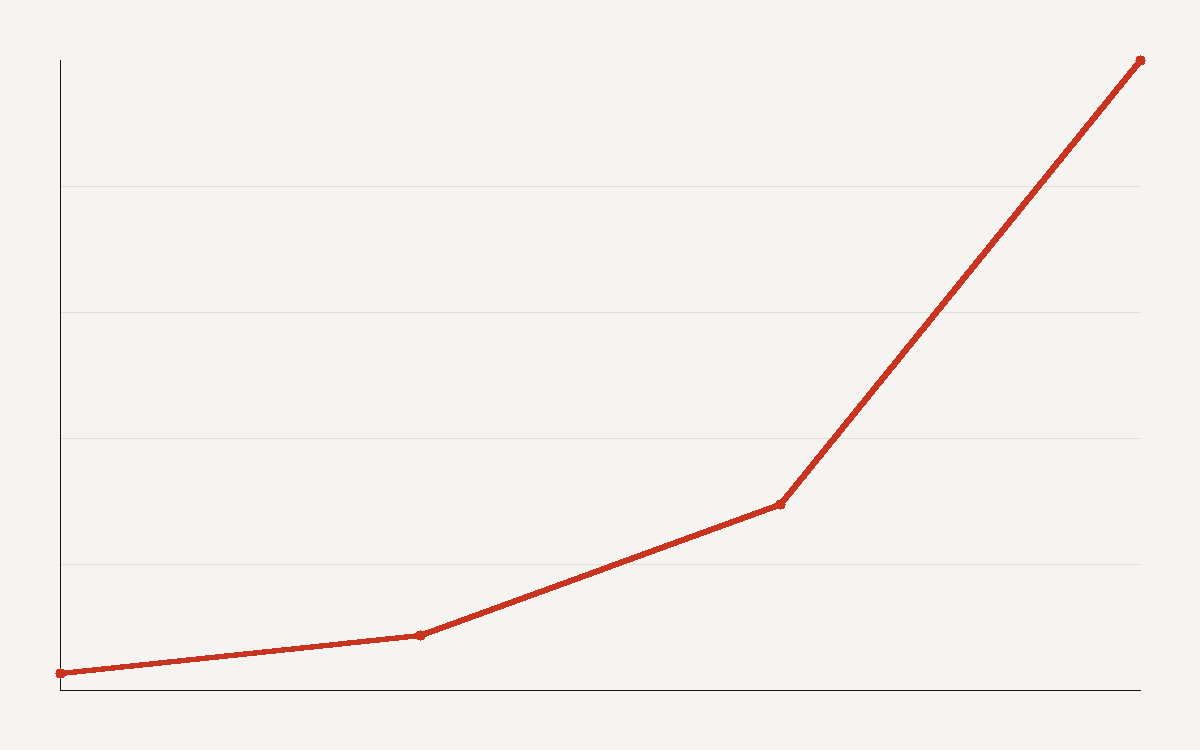

Compute is compounding

The stock of AI compute, charted above, is growing about 3.4 times per year, doubling roughly every seven months since 2022. Training compute for frontier language models has climbed about 5 times per year since 2020, while the cost of those training runs rises about 3.5 times per year and power use roughly doubles annually. Stack those curves and the shape of a frontier budget stops being a research line item and becomes an infrastructure bill: data centres, power contracts, and silicon dwarf the salaries of the people writing the models.

Why this favours incumbents

When the marginal advantage comes from owning power and silicon, geography and balance sheets decide who competes. The United States holds about three-quarters of global GPU cluster performance today. Gigawatt-scale sites take around two years to build, which turns AI strategy into a real-estate and energy problem as much as a research one.

What to watch

The open question is whether capability keeps tracking this spend. The scaling curve has held so far, and Epoch argues the trend can continue through 2030. If returns flatten before the concrete is poured, some of these commitments will look very large in hindsight. The underlying numbers are tracked in Epoch AI's trends dashboard.

Capital intensity changes the research culture

When a training run depends on gigawatts and billions of dollars, research becomes tied to capital allocation. The lab still needs scientists, but the frontier experiment also needs power contracts, procurement teams, construction partners, and finance committees. That changes which ideas get tested. The best proposal is no longer only the most elegant one. It is the one that can justify scarce compute on a schedule.

This pressure can narrow the field. Smaller teams may produce important algorithmic ideas, but they may need a large partner to test those ideas at full scale. Large companies can run more frontier experiments, collect more failure data, and turn infrastructure into a learning advantage. The gap is not only the size of the cluster. It is the feedback loop the cluster permits.

There is a counterweight. High capital intensity makes efficiency research more valuable. Any method that reduces training compute, improves data quality, raises utilization, or transfers capability to smaller models can save enormous amounts of money. The infrastructure race therefore increases the prize for better algorithms even as it raises the cost of testing them.

Why consultants follow the spend

Large capital programs create advisory markets. Companies spending billions on AI infrastructure need forecasts, procurement advice, power strategy, risk models, governance plans, and board narratives. The consultant promise is to turn a technical arms race into an investment plan. Some of that work is useful. Some of it will be expensive storytelling around uncertain curves.

The risk is that AGI language can blur ordinary capital discipline. A project that would be questioned as a data-center investment may look inevitable when it is framed as a step toward general intelligence. Investors and boards should still ask normal questions: what capacity is committed, what demand is already contracted, what utilization is assumed, and what happens if model returns slow?

Those questions do not dismiss the technology. They protect the company from mistaking momentum for proof. Frontier AI may justify unusually large bets, but large bets still need milestones that can be measured before the full bill is spent.

The user-facing consequence

Most customers will never see the gigawatt bill directly. They will see it in product packaging. Providers will push subscriptions, usage tiers, committed spend contracts, and enterprise bundles that help finance fixed infrastructure. They will also try to move routine work onto cheaper models so premium capacity is reserved for high-margin tasks.

That means buyers should ask where their workload sits in the provider's cost stack. A feature that uses commodity inference should not be priced like a frontier reasoning product. A feature that depends on scarce premium capacity may face throttling, higher minimums, or stricter terms during demand spikes.

The infrastructure story therefore matters even for ordinary software buyers. It explains pricing, availability, vendor concentration, and the pressure to commit early. The model may be the visible product, but the power contract is increasingly the economic engine behind it.

How to judge the promise

The serious question is whether each new dollar of infrastructure produces a larger base of paying capability. That can happen through better models, cheaper serving, larger customer volume, or more valuable product bundles. If the spend only produces impressive demos, the economics weaken. If it produces dependable services that customers use daily, the gigawatt bill becomes easier to defend.

Boards and buyers should therefore ask for milestones that connect capacity to use. How much of the planned compute is contracted? Which products depend on it? What utilization is assumed? Which workloads can move to cheaper models if frontier capacity is scarce? Those questions turn AGI promises into operating assumptions that can be checked.