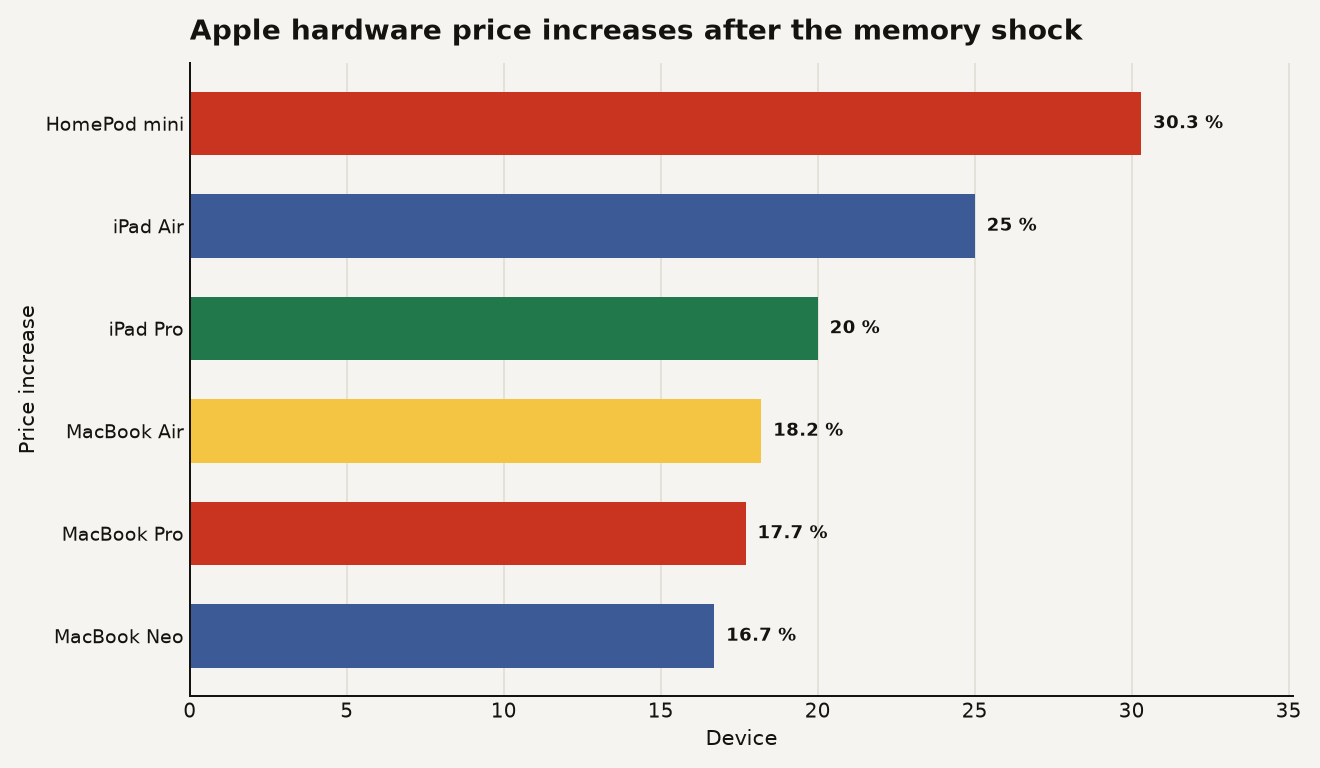

The AI boom has finally found a clean consumer billing surface: the checkout page for normal hardware. Apple is raising prices on Macs, iPads, and home devices after months of memory market stress, and the Apple AI price hike is bigger than a nuisance fee. The sharpest small-product move is the HomePod mini, which went from $99 to $129, a 30.3 percent jump by Data Today's calculation from reported Apple store price changes.

Apple's explanation is simple enough. AI data centers are swallowing memory and storage supply, suppliers can charge more, and consumer device makers have to decide whether to eat the bill or pass it on. Apple told MacRumors on June 25, 2026 that it had never seen a component price increase happen "this much, this quickly".

That is true as far as the component market goes. It is also too tidy. Apple reported $111.184 billion in revenue and $29.578 billion in net income for the quarter ended March 28, 2026, according to its own Q2 2026 consolidated financial statements. A company with $29.6 billion of quarterly profit has options, even when DRAM gets ugly.

The better read: AI infrastructure has turned memory into a market-wide tax, but Apple is choosing how much of that tax lands on customers. If you build hardware, buy fleet laptops, or run a device-heavy business, this is your warning that AI capex is no longer somebody else's spreadsheet.

How much did Apple actually raise prices?

The price changes landed across the parts of Apple's catalog most exposed to RAM and storage: Macs, iPads, and home hardware. Tom's Hardware listed the MacBook Neo moving from $599 to $699, the MacBook Air from $1,099 to $1,299, the MacBook Pro from $1,699 to $1,999, the iPad Pro from $999 to $1,199, and the iPad Air from $599 to $749 in its June 25, 2026 price table. MacRumors reported that Apple raised prices on 14 product lines, with the increases ranging from $30 for HomePod mini to $1,300 for Mac Studio in its coverage of Apple's statement.

The chart below converts the cleanest entry-level moves into percentage increases. The headline is awkward for Apple: the cheapest, least glamorous products saw some of the highest percentage jumps.

The HomePod mini rose 30.3 percent, the iPad Air rose 25.0 percent, and the iPad Pro rose 20.0 percent by Data Today's calculation from the old and new prices reported by Tom's Hardware. The MacBook Air increase works out to 18.2 percent, while the entry MacBook Pro moved 17.7 percent and the MacBook Neo moved 16.7 percent from the same price table.

The iPhone stayed out of this round, at least publicly. Axios reported on June 25, 2026 that Apple did not include the iPhone in the announced price increases, while the company said it needed to "begin" raising prices on some products in its statement to the press. That word matters. Begin is a runway, not a full stop.

Is the AI memory squeeze real?

Yes. The memory squeeze is real, and it is bigger than Apple.

TrendForce said conventional DRAM contract prices were forecast to rise 55 percent to 60 percent quarter over quarter in the first quarter of 2026, with suppliers reallocating advanced process nodes and new capacity toward server and HBM products for AI demand in its January 5, 2026 memory market report. The same report forecast NAND Flash prices up 33 percent to 38 percent quarter over quarter, with client SSD prices expected to rise by at least 40 percent as suppliers shifted output toward data center SSDs.

That is the commodity layer behind Apple's story. HBM, server DDR5, RDIMMs, SSDs, and mobile DRAM do not sit in sealed universes. The wafer starts, packaging capacity, supplier attention, and long-term agreements all collide. AI customers with giant purchase commitments get priority. Everyone else negotiates after the big buyers have taken their seats.

TrendForce's June 2, 2026 HBM analysis is even more direct about the crowding effect: it estimated HBM wafer input among the top three DRAM suppliers would rise from 18 percent of total DRAM wafer input at the end of 2025 to 22 percent at the end of 2026 and 30 percent at the end of 2027 in its HBM pricing report. That is supply moving toward accelerators and away from the memory diet that keeps laptops, phones, consoles, routers, and embedded devices boringly affordable.

Micron's numbers show why suppliers like this world. Micron reported fiscal third-quarter 2026 revenue of $41.456 billion and a gross margin of 84.6 percent in its official Q3 2026 results. Its Cloud Memory Business Unit alone posted $13.769 billion of revenue and an 83 percent gross margin in the same release.

When a supplier can sell scarce memory into a data center order book at rich margins, your laptop refresh is a less thrilling customer.

Why does this matter if you build or buy technology?

The easy consumer reaction is irritation. The builder reaction should be planning.

If you are running a software team, the price of RAM is now part of your AI roadmap even if you never touch a GPU cluster. Fleet refreshes get more expensive. Developer laptops with enough unified memory for local models get harder to standardize. Edge products with embedded storage become less forgiving. Any roadmap that assumes hardware gets steadily cheaper by default deserves a hard look in July 2026.

This is the same supply chain lesson behind Apple's memory policy fight: memory used to feel like a procurement detail, and now it behaves like strategic infrastructure. Apple can talk about unavoidable costs, but the market is really repricing priority access.

For your budget, that means four things:

- Device refresh cycles stretch. A $200 MacBook Air increase looks small beside cloud GPU bills, but multiplied across 500 employees it becomes a $100,000 procurement event.

- Local AI gets a hardware toll. More on-device inference means more RAM and storage per endpoint, just as those components are being bid up by data centers.

- Small hardware margins get squeezed first. A startup shipping a smart camera, medical device, kiosk, or robotics controller has less pricing power than Apple.

- Cloud AI costs can leak into non-cloud goods. The AI team may own the token bill, but the finance team will see the memory bill in laptops, test devices, and customer hardware.

Microsoft's Xbox announcement makes the spillover hard to dismiss. Xbox said console prices would rise by $100 for 512 GB models and $150 for 1 TB models starting August 1, 2026, because console storage and memory prices had increased by more than 2.5 times in its Xbox Wire update. Xbox also said it expected another doubling by fall 2027 in the same update.

Consoles are useful evidence because they are brutally cost-sensitive. Microsoft cannot dress up a price hike as a luxury upgrade. It is a bill of materials story, and the bill is moving.

Could Apple have absorbed more of the hit?

Apple could have absorbed more than many hardware companies. That does not mean it should absorb all of it forever, but the financial cushion is large.

Apple's Q2 2026 financial statements show products revenue of $80.208 billion and product cost of sales of $49.179 billion, which implies a product gross margin of about 38.7 percent by Data Today's calculation from Apple's own figures. Total company gross margin was about 49.3 percent in the same quarter, using gross margin of $54.781 billion on total net sales of $111.184 billion.

Those margins do not prove Apple is gouging. They do prove Apple is not a console maker trapped at the edge of a loss-leading hardware model.

This is where the shareholder story enters. Apple's pricing power is part of the brand, and Wall Street rewards it for protecting margin. If memory costs rise and Apple eats them, investors ask whether the hardware business is structurally less profitable. If Apple raises prices and demand holds, investors see proof that the brand can pass through a shock. Customers get to audition for the role of margin stabilizer.

For builders, the lesson is colder than the consumer complaint. The companies with distribution, brand, and ecosystem lock-in can pass through AI infrastructure inflation. The companies without those assets will redesign products, cut memory configurations, delay launches, or accept lower margins. If your moat depends on cheap hardware assumptions, AI capex is already poking it.

What should you do before this reaches your roadmap?

Treat memory as a strategic input for the next 18 months, not a commodity line item that procurement fixes at the end.

Start with configurations. If your team buys laptops for AI-assisted development, stop defaulting to the lowest RAM tier and pretending the upgrade decision is personal preference. Local coding agents, embedding workflows, browser-heavy dashboards, and on-device model tests all punish under-specced machines. Buying too little memory in 2026 can become a hidden productivity tax in 2027.

Then audit your product bill of materials. Any device that ships with DRAM, NAND, or SSD capacity needs a version of the question cloud teams ask about GPUs: what happens if the part doubles, arrives late, or gets allocated to a larger buyer? TrendForce's forecast that HBM wafer input could hit 30 percent of top-supplier DRAM wafer input by the end of 2027 is a useful stress-test input from its June 2026 report.

The practical moves are plain:

- Lock supply earlier for critical SKUs, especially if you ship physical products in Q4 2026.

- Offer fewer memory configurations if complexity creates exposure without meaningful customer value.

- Make local AI features degrade gracefully on lower-memory devices.

- Separate unavoidable component pass-through from opportunistic price increases in customer messaging.

- Revisit cloud-versus-edge AI assumptions when both sides depend on the same memory supply chain.

That last point is the subtle one. A lot of AI product strategy assumes a clean tradeoff: run in the cloud for scale, run on-device for privacy or latency. The memory squeeze makes the tradeoff messier. Cloud inference eats HBM and server DRAM. On-device inference eats LPDDR, NAND, and premium endpoint configurations. The same AI boom taxes both paths, just through different vendors.

The bill always finds an interface

Apple did not create the AI memory squeeze by itself. It also did not wake up helpless.

The useful lesson from the Apple AI price hike is that infrastructure costs rarely stay inside infrastructure. They travel until they find an interface with pricing power. This week, that interface was a MacBook checkout page.

If you are building in AI, assume your customers will eventually ask the same question Apple customers are asking now: why am I paying for someone else's data center race? Have a better answer than "component costs."

Sources

- Apple: Q2 2026 consolidated financial statements

- MacRumors: Apple explains why it raised prices on 14 products today

- Tom's Hardware: RAM crisis bites Apple as Mac and iPad price rises arrive

- TrendForce: Memory makers prioritize server applications in 1Q26

- TrendForce: Tight DRAM supply gives suppliers greater pricing power in HBM

- Micron: Fiscal Q3 2026 results

- Xbox Wire: Updated Xbox console prices

- Axios: Apple price increases hit Mac and iPad in AI ripple effect