The first serious retail fight over AI agents will not be won by the prettiest storefront. It will be won by the checkout flow that a machine can trust, parse, and complete without getting stuck on a coupon modal from 2018.

Agentic commerce is now a payments problem, not just a chatbot demo.

Visa announced on June 10, 2026 that it is partnering with OpenAI to bring Visa payments into agentic commerce across OpenAI experiences. The key phrase is agentic commerce: a system where an AI agent can help a user discover, compare, and complete a purchase under defined permissions. Visa says the deal will use its network, credentialing, tokenization, and risk capabilities, and its own Intelligent Commerce page puts the network footprint at 4.8 billion payment credentials, more than 175 million merchant locations, and more than 300 billion transactions processed annually through Visa’s network.

That scale is the story. OpenAI already turned ChatGPT into a shopping surface in 2025 with Instant Checkout and the Agentic Commerce Protocol, initially for U.S. Etsy sellers and later with Shopify merchants planned. Visa’s move aims at the next bottleneck: turning agent initiated buying from a platform specific checkout trick into something issuers, merchants, fraud teams, and developers can recognize.

The overhyped version says ChatGPT will now roam the web with your card and buy whatever the prompt suggests. The useful version is narrower and more important: payment networks are building the trust layer for AI agents, and retailers that still treat their website as the only product interface are about to discover that a bot does not care about hero images.

What did Visa and OpenAI actually announce?

Visa’s announcement is not a new shopping chatbot. It is infrastructure for a checkout path where the user gives permission, an AI agent initiates a purchase, and the payment credential carries enough context for the network and issuer to evaluate the transaction.

According to Visa’s June 10 announcement, the partnership will integrate Visa payment capabilities into OpenAI experiences so developers and merchants can accept Visa payments initiated by agents. Visa says transactions will operate within user permissions, policies, and controls such as spending limits, merchant categories, or required approvals. It also says those transactions will use tokenized Visa credentials plus real-time authorization and fraud monitoring.

Read that carefully. The product is not just “let the model buy stuff.” The product is scoped delegation.

That matters because today’s e-commerce stack assumes a human is present at three points:

- Product discovery, where the user sees search results, ads, reviews, and comparison pages.

- Checkout intent, where the user clicks a button and confirms shipping, taxes, payment, and price.

- Post-purchase support, where the user handles returns, refunds, and disputes.

Agents scramble that sequence. A buyer might ask ChatGPT for “the cheapest reliable carry-on under $180 that arrives by Friday,” then let the agent choose between five merchants. The product page may never get a human visit. The ad may never render. The discount banner may never load. The merchant either exposes clean machine-readable data and a reliable checkout path, or it is invisible at the moment of purchase.

Visa is also trying to make the agent legible to the rest of the payment system. At its 2026 Payments Forum, Visa announced Agent Score, an Agentic Directory, token enhancements, and a Large Transaction Model trained on billions of transactions to improve fraud detection and authorization performance. In the same Payments Forum release, Visa said tokens will carry more detail about transaction type, token use, and who is making the payment.

That is the boring machinery behind the flashy headline. Boring machinery is usually where the margin is.

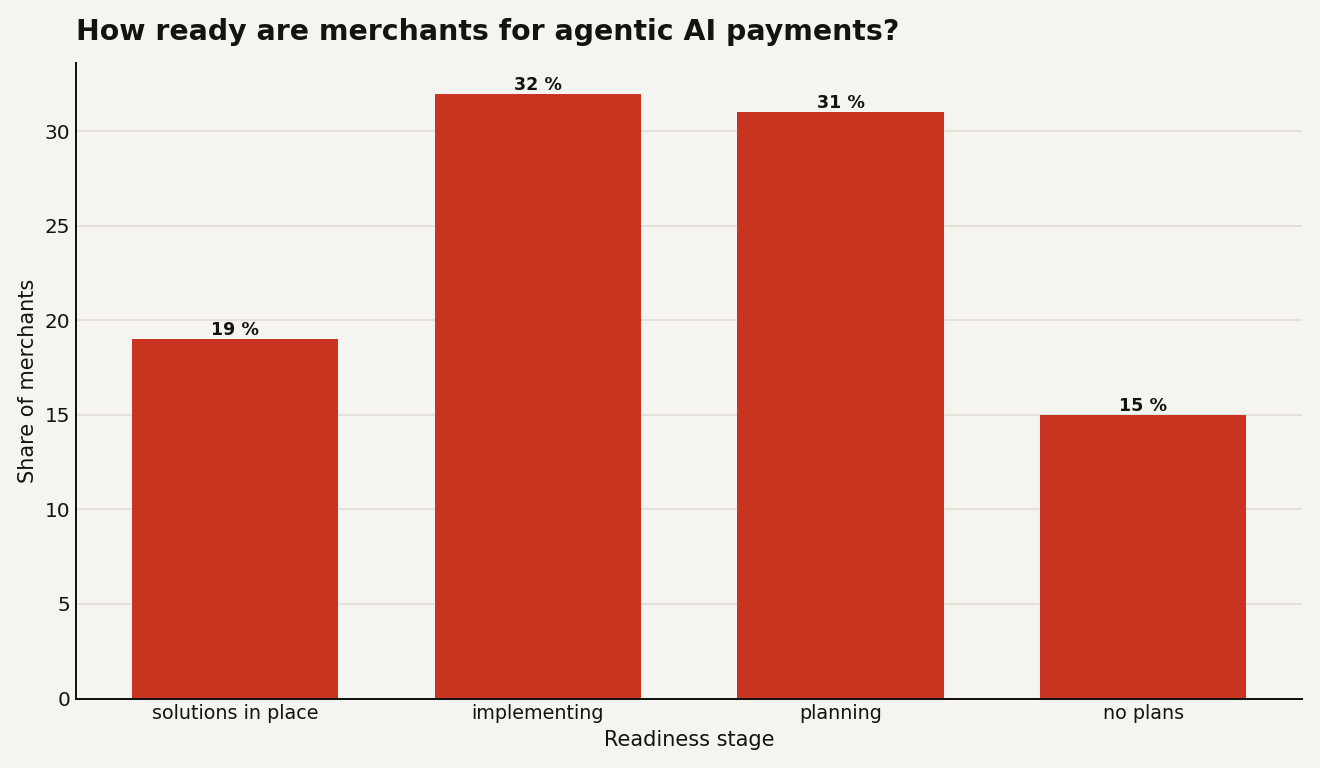

How ready are merchants for agentic commerce payments?

Visa’s own merchant data says the market is not ready yet, but it is moving faster than a novelty cycle. In the 2026 Global eCommerce Payments and Fraud Report, Visa defines agentic AI payments as e-commerce payments initiated by AI assistants or applications on behalf of human consumers. The survey found that 19 percent of merchants already have a plan and solutions in place to accept agentic AI payments.

The chart below is the adoption curve hiding under the press release. Another 32 percent of merchants said they were in early implementation, 31 percent were planning or exploring, and 15 percent had no plans or solutions in place.

The split is important because it exposes the near term product gap. If you are a merchant, the competitive threat is not “everyone will have agent checkout tomorrow.” It is that half the market is either already set up or implementing, while your bot wall, brittle checkout, and incomplete product feed may still be optimized for a browser session.

Visa’s earlier pilot update gives a second signal. In January 2026, the company said more than 100 partners were working across the commerce ecosystem, over 30 were building in the Visa Intelligent Commerce sandbox, and over 20 agents and agent enablers were integrating directly with Visa Intelligent Commerce. Visa also said those collaborations had produced hundreds of controlled, real-world agent initiated transactions.

That is not mass adoption. It is enough to start hardening standards, failure modes, and merchant expectations before the 2026 holiday season. If your roadmap still treats agent traffic as a bot management problem only, you may block your next buyer at the edge.

OpenAI’s own design points in the same direction. Its Instant Checkout launch said ChatGPT product results are organic and unsponsored, and that when multiple merchants sell the same product, ChatGPT considers availability, price, quality, whether the merchant is the primary seller, and whether Instant Checkout is enabled. The uncomfortable phrase for retailers is “whether Instant Checkout is enabled.” Distribution advantage can become protocol advantage very quickly.

Why does this change the builder’s roadmap?

Because the buyer interface is moving from web pages to endpoints.

If you build commerce software, the old funnel telemetry starts to lose signal. A human session has scroll depth, dwell time, click paths, abandoned carts, heat maps, and retargeting events. An agent session may have none of that. It can query a product feed, call a checkout endpoint, receive a deterministic response, and leave.

The codebase consequence is simple: your product catalog, checkout, order state, and payment logic need to be API first in practice, not just in a slide. OpenAI’s Agentic Commerce Protocol documentation says merchants implementing checkout must expose REST endpoints for creating, updating, completing, canceling, and retrieving checkout sessions. It also says responses must return a rich cart state with items, pricing, taxes, fees, shipping, discounts, totals, and status.

That is not SEO copy. That is contract design.

The business consequence is sharper. The merchant’s brand may no longer be the thing a user browses first. The user’s agent may rank options against constraints. Your advantage shifts from merchandising psychology to machine usable truth:

- Catalog quality: complete attributes, normalized variants, stock status, delivery dates, return windows, and warranties.

- Checkout reliability: idempotent endpoints, clear error handling, safe retries, and consistent order state.

- Price computability: taxes, shipping, discounts, loyalty benefits, and fees visible before the final authorization.

- Trust signals: agent verification, cryptographic signatures, token context, fraud controls, and dispute records.

- Post-purchase automation: return labels, refund rules, support status, and replacement options available to agents.

If you sell a commodity product, this is brutal. A product page with better photography will matter less when the buyer agent is optimizing price, arrival date, reviews, and return terms. If you sell a differentiated product, this is still risky because the agent cannot choose what it cannot understand. Your moat has to survive translation into structured data.

This is also where the protocol fight matters. OpenAI and Stripe’s Agentic Commerce Protocol is one lane. Google announced AP2 in September 2025 as an open protocol for agent led payments built with more than 60 organizations, including Adyen, American Express, Coinbase, Etsy, Mastercard, PayPal, Salesforce, and Worldpay. Mastercard announced Agent Pay in April 2025 with agentic tokens and partnerships including Microsoft, IBM, Braintree, and Checkout.com.

You do not need to bet your whole company on one protocol this quarter. You do need to stop building checkout as if the only caller is a React frontend.

If you have been following the protocol layer through our MCP explainer for data engineers, the shape should look familiar. Agents need tools. Tools need schemas. Schemas need permissions. Permissions need logs. Payments add a nastier requirement: when the agent is wrong, someone still gets a chargeback, a support ticket, or a lawsuit.

What should merchants and developers do now?

Start with a narrow assumption: agentic commerce will hit high intent, low ambiguity purchases first. Reorders, replacement parts, groceries, travel add-ons, office supplies, simple apparel, subscriptions, and B2B procurement are better early targets than emotionally loaded, high consideration purchases.

Then audit your stack against four boring tests.

First, can an agent understand what you sell without seeing your UI? Pull 50 SKUs and inspect the fields an agent would need: size, compatibility, delivery date, warranty, return rules, country restrictions, materials, subscriptions, and total cost. If the critical buying criteria live only in images, PDFs, or marketing copy, your feed is underbuilt.

Second, can an agent complete checkout without improvising? The Agentic Commerce Protocol spec requires HTTPS and JSON, request signatures, timestamps, API versions, idempotency, input validation, and safe retries. Those are table stakes for normal commerce reliability. With agents, they become discoverability features because a checkout that fails unpredictably will be routed around.

Third, can you prove intent after the fact? Visa’s token direction is to carry richer context about who or what initiated the transaction, where the token was used, and what type of transaction occurred. Google’s AP2 frames the same problem as authorization evidence: today’s payment systems assume a human clicks buy, while agents break that assumption. Your logs should be able to answer a dispute with more than “the API returned 200.”

Fourth, can your support operation talk to another agent? If a user says, “Return the headphones because they do not meet the battery life I asked for,” the next interaction may be agent to merchant API, not angry human to chatbot. If your return policy is a wall of text and your support status is trapped in a ticketing portal, your agent experience ends after purchase.

For a builder, the near term roadmap should look like this:

- Instrument agent traffic separately from crawler traffic and human sessions.

- Add structured product fields for the top 20 decision criteria in your category.

- Make checkout session APIs idempotent and observable.

- Store authorization context, cart state, model or agent identifier where available, and user approval artifacts.

- Test failure cases with adversarial prompts, expired stock, partial discounts, address errors, and refund requests.

Do not overbuild a moonshot “AI store.” Build boring agent compatibility into the commerce path you already trust.

What could still break before this becomes normal?

Three things can slow this down.

The first is user trust. Visa said in January 2026 that 47 percent of U.S. shoppers used AI tools for at least one shopping task, from price comparisons to personalized recommendations. That is not the same as letting an agent spend money. Moving from “find me options” to “buy the best one” is a psychological jump, especially when returns, warranties, and fraud are involved.

The second is protocol fragmentation. ACP, AP2, Visa’s Trusted Agent Protocol, Mastercard Agent Pay, and merchant specific APIs may all coexist. That is normal in payments, but it increases integration cost. The winning architecture for most merchants will be an abstraction layer that can accept multiple agent identities, checkout schemas, and delegated payment tokens without turning the backend into spaghetti.

The third is liability. Tokenization and spending controls reduce blast radius, but they do not eliminate bad decisions. An agent can still choose the wrong size, misunderstand a review, miss a shipping cutoff, or get steered by hostile content. Visa’s controls help with payment authorization and fraud monitoring. They do not magically solve product truth.

That is why the best near term bet is not full autonomy. It is supervised autonomy with hard caps: approved merchants, category limits, explicit confirmation above a threshold, and a clear audit trail. In other words, let the agent do the work, but do not let it become the finance department.

The real shift is not that ChatGPT can buy a suitcase. It is that commerce is getting a new user class: software with a mandate, a budget, and no patience for your frontend.

Sources

- Visa: Visa Partners with OpenAI to Power the Next Generation of AI Commerce

- Visa: Visa Announces New AI, Stablecoin and Token Innovations to Power Intelligent, Programmable Commerce at Visa Payments Forum

- Visa: Visa Intelligent Commerce

- Visa: Visa and Partners Complete Secure AI Transactions, Setting the Stage for Mainstream Adoption in 2026

- Visa: 2026 Global eCommerce Payments and Fraud Report

- OpenAI: Buy it in ChatGPT: Instant Checkout and the Agentic Commerce Protocol

- Agentic Commerce Protocol: Agentic Checkout Specification

- Google Cloud: Powering AI commerce with the new Agent Payments Protocol

- Mastercard: Mastercard unveils Agent Pay, pioneering agentic payments technology to power commerce in the age of AI