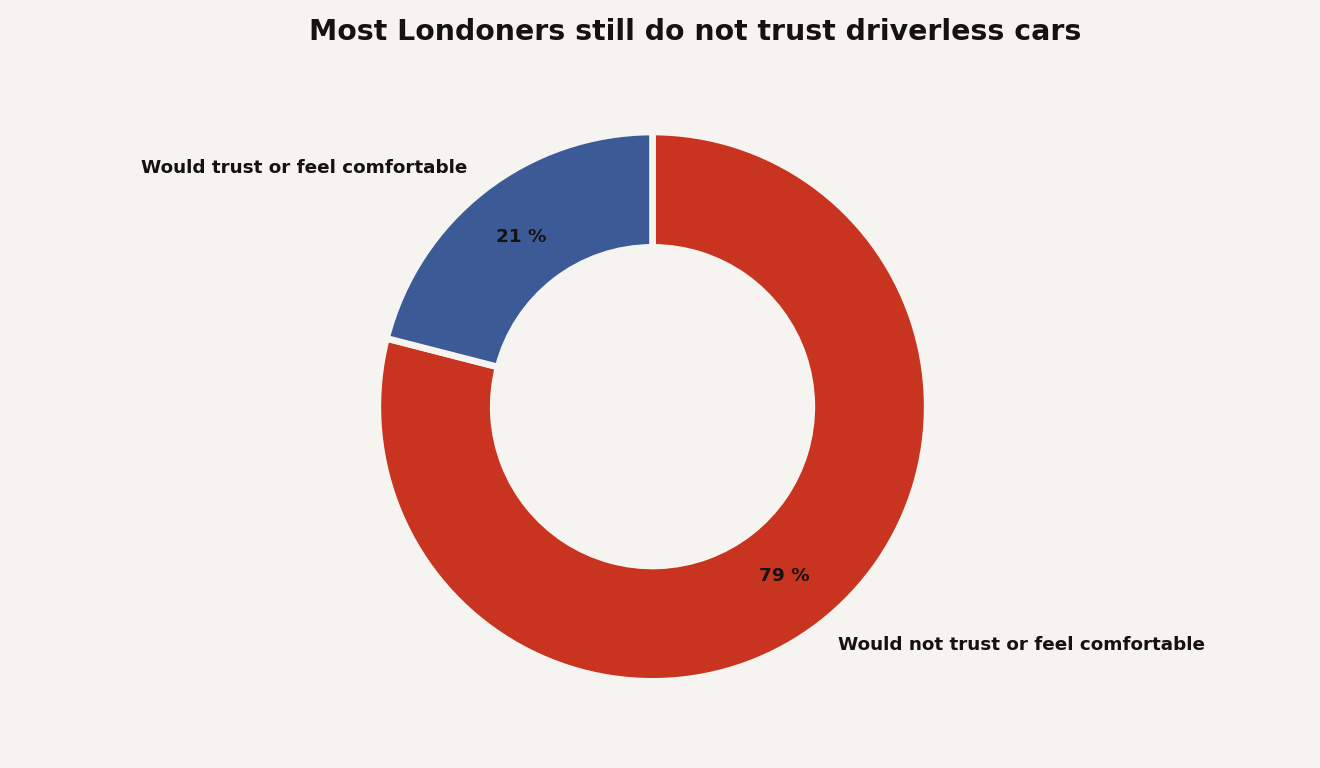

The London robotaxi race is starting with a button in the Uber app, not with a fleet roaring across the capital. That is the right level of drama. Uber and Wayve are asking riders to join an interest list for autonomous rides in London, but the most useful number is not the launch date. It is 79 percent: the share of Londoners who would not trust or feel comfortable in a driverless car, according to a London Assembly summary of HPI survey findings.

That gap between product readiness and public trust is the whole story. A London robotaxi is no longer a speculative demo video. It is becoming a regulated ride-hailing product with pricing, routing, customer support, vehicle operations, safety cases, local politics, and a cancel button.

Uber’s move matters because London is not Phoenix with worse weather and better pubs. It is one of Uber’s most important international markets, one of the world’s most scrutinized taxi cities, and a brutal test bed for autonomy: narrow roads, buses, cyclists, tourists, roadworks, delivery riders, and the occasional pedestrian who treats a zebra crossing like a force field. If Wayve’s AI-first driving system works here, the company gets a much stronger story than another closed-course milestone.

The catch is simple. This is a launch signal, not a finished robotaxi business. The Verge reported that the first London fleet is expected to start with a mid-to-high single-digit number of cars, and the early rides will still have a safety driver behind the wheel. That is not a failure. It is the honest version of the product.

What did Uber and Wayve actually open in London?

Uber opened an interest list on June 8, 2026 for UK users who want a chance to be matched with a Wayve autonomous vehicle when the London service launches. Reuters reported that riders will be able to sign up from Monday, with launch timing dependent on regulators and expected “in the coming months” by the companies.

The user flow is intentionally boring. In the Uber app, a rider opts into autonomous vehicles under ride preferences. If matched later, the rider can accept the autonomous vehicle or switch to a conventional ride. Uber says the autonomous option will not cost extra when requested through familiar products such as UberX, Uber Electric, or Uber Comfort.

That detail matters more than the branding wrap on the car. Uber is not asking Londoners to download a new app, learn a new marketplace, or pay a novelty premium. It is trying to make the robotaxi feel like another supply type inside Uber’s existing demand machine. For a consumer product, that is the shortest path from “weird” to “normal.”

Wayve supplies the driving system. Uber supplies the demand, rider experience, and operating layer. The London vehicle shown publicly is a Ford Mustang Mach-E with cameras and radar, and Reuters reported that the system processes sensor data in the vehicle. Wayve’s Kaity Fischer told Reuters the company has tested the technology on London roads since 2018.

This is also why the word “robotaxi” needs an asterisk for the first phase. The early London rides are autonomous in the sense that the system drives the route, but they are not fully driverless. A trained operator sits behind the wheel. If you are building on top of autonomy, that distinction is not pedantry. It changes the cost model, the safety case, the customer promise, and the regulatory burden.

Uber has been preparing to be the distribution layer for many autonomy stacks, not the owner of one magic stack. In February 2026, the company launched Uber Autonomous Solutions, describing services for training data, mapping, rider experience, support, and fleet operations. Dara Khosrowshahi put the strategic frame plainly: “meaningful commercialization will take much longer.”

That is a CEO quote worth taking seriously. The company is selling patience while opening the waitlist.

How much trust does a London robotaxi have to earn?

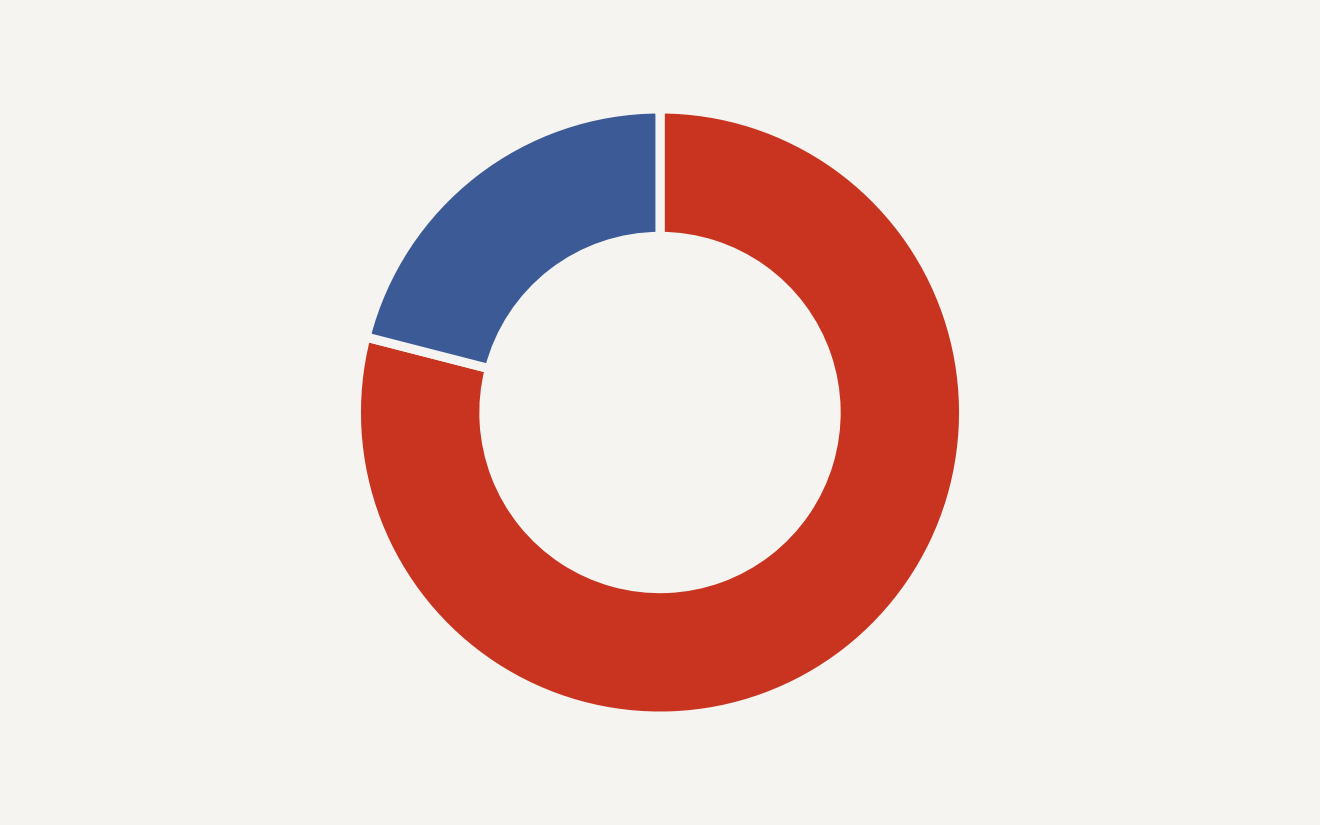

The chart below is the uncomfortable part of the launch. The London Assembly’s Transport Committee cited HPI research finding that 79 percent of Londoners would not trust or feel comfortable travelling in a driverless car, while only 21 percent would. That is not a marketing problem. That is an adoption bottleneck.

The interest list is Uber’s first data product here. It gives Uber and Wayve a demand signal before they have meaningful supply. Which boroughs produce sign-ups? Which rider segments opt in? Do people accept the autonomous match at 8 pm but reject it at 1 am? Do airport trips behave differently from short hops? Those answers will shape the operational design domain faster than a strategy deck.

The same London Assembly document, published on May 22, 2026, says several autonomous passenger vehicle trials are underway in London in 2026, with operators aiming for commercial services by the end of the year. It also says Waymo’s London testing fleet comprises 24 vehicles, while other operators have not confirmed planned fleet sizes.

That puts Uber and Wayve in a strange position. They are early enough to define the first consumer experience, but not early enough to avoid comparison. Waymo is already the reference point. The London Assembly notes that Waymo reports approximately 500,000 paid rides every week using more than 3,000 vehicles across ten US cities. A London trial with fewer than ten cars will not compete with that scale. It will compete with that expectation.

This is where hype gets sloppy. A rider does not care whether the model generalizes across continents if the car takes six minutes to pull over safely, cannot stop near a busy station, or hands the route back to a human operator. The benchmark is not a conference demo. The benchmark is a minicab that arrives in four minutes and does not make you think about operational design domains.

For builders, the trust chart should look familiar. New AI products often fail in the gap between benchmark performance and workflow trust. We saw the same pattern in agent systems, where impressive isolated capabilities did not translate cleanly into reliable production behavior, as covered in Data Today’s piece on why agentic AI projects get cancelled before shipping. Autonomy is the physical-world version of that problem, with insurance, road users, and city hall in the loop.

Why does this matter if you are building or buying AI?

Because robotaxis are becoming one of the cleanest tests of embodied AI commercialization. Wayve is not just selling “self-driving.” It is selling a thesis: train a general driving model from real-world data, avoid brittle city-by-city hand engineering where possible, and license the AI Driver across vehicles and markets.

Wayve’s funding round shows how much capital is chasing that thesis. In February 2026, Wayve said it had raised a $1.2 billion Series D and secured $1.5 billion of capital for commercial rollout, bringing the company to an $8.6 billion post-money valuation. The company also said it drove zero-shot in more than 500 cities across Europe, North America, and Japan in a single year.

Those numbers are not proof that Wayve can run London profitably. They are proof that investors, automakers, and platforms believe autonomy is shifting from bespoke robotics to AI software distribution. That changes the competitive map.

For you, the consequences break down like this:

- If you build AI products, watch the safety case, not the launch video. The hard work is instrumentation, escalation, human override, and audit trails.

- If you run a marketplace, Uber’s playbook is clear: own demand, payments, support, and routing while letting multiple suppliers compete underneath.

- If you buy AI systems, treat “autonomous” as a deployment mode, not a feature label. Ask what happens when the system leaves its approved operating conditions.

- If your moat is local operations, this is the warning shot. AI does not remove operations. It makes operations the thing that decides whether the AI reaches customers.

That last point is underrated. Uber’s advantage in London is not that it has the best driving model. It is that it already knows where riders are, where trips fail, where pickups are messy, and how to refund an annoyed human at scale. In its Autonomous Solutions announcement, Uber says its data-collection fleet spans thousands of specially equipped vehicles across dozens of cities and has captured millions of diverse multi-sensor miles.

Wayve’s advantage is different. In its Series D announcement, the company says its system runs on onboard compute and embedded sensors and does not rely on high-definition maps or location-specific engineering. If that works under London conditions, the company can argue that it has a more portable autonomy stack than older map-heavy approaches.

The business question is whether those two advantages multiply or grind against each other. Uber wants optionality across Wayve, Waymo, WeRide, Nvidia, Nuro, Avride, Baidu, and whoever else can pass the safety and economics bar. Wayve wants distribution without becoming a commodity supplier. That tension will not show up in the first passenger selfie. It will show up in contracts, margins, and who owns the rider relationship.

What does the UK regulatory path actually allow?

The UK has moved faster than many people expected, but the legal path is still staged. The Department for Transport’s consultation on Automated Passenger Services says the permit scheme is intended to apply for initial pilots from spring 2026 and for deployments after full implementation of the Automated Vehicles Act in the second half of 2027.

That means London is not simply “turning on” driverless taxis. The government is building a bridge from supervised trials to driverless passenger services. The same consultation says permits are meant to cover services operating without a human driver or trials developing vehicles that might be used without a driver.

The applicant guidance is even more revealing. GOV.UK says the remaining provisions of the AV Act are due to come into force in late 2027, and it describes vehicle listing, special orders, registration, and automated passenger service permits as part of the path to legal deployment.

For Uber and Wayve, regulation is not a checkbox at the end of engineering. It is part of the product surface. The app has to explain the ride. The car has to behave around emergency services. The operator has to document safety. Local authorities and TfL have to understand where the vehicles operate and how they affect other road users.

That is why this launch will be more constrained than the word “robotaxi” suggests. A geofence is a product decision. Pickup points are a product decision. Weather limits are a product decision. The safety driver’s role is a product decision. None of these are glamorous, but they decide whether riders trust the system by trip five.

The politics also matter. London’s transport goals include Vision Zero, a traffic reduction target of 10 to 15 percent, and a target for 80 percent of trips to be made by active modes or public transport, according to the London Assembly. Robotaxis that add empty vehicle miles or pull riders from buses will face a different argument than robotaxis that reduce dangerous driving or fill late-night transit gaps.

What should builders watch next?

Start with the unsexy metrics. Fleet size, intervention rate, trip completion rate, acceptance rate, pickup success, and how quickly Uber lets a rider switch back to a human driver will tell you more than another “AI driver handles complex streets” clip.

The first milestone is whether Uber and Wayve move from an interest list to paid public rides in 2026. The second is whether the service grows beyond a handful of cars. The third is whether the safety driver disappears under the UK’s permitting framework. Until then, this is a supervised autonomy product with real commercial intent, not a full driverless network.

Also watch Uber’s portfolio strategy. In March 2026, Uber, Wayve, and Nissan announced a Tokyo pilot planned for late 2026 as part of a Wayve and Uber rollout across 10 plus cities, including London. Five days later, Uber and Nvidia announced a plan to launch Nvidia software-driven autonomous vehicles starting in Los Angeles and San Francisco in the first half of 2027, then scale across 28 cities globally by 2028.

That is not one bet. It is a marketplace hedging against the autonomy stack being late, local, or uneven.

For founders, that is the practical lesson. If the model is uncertain, own the workflow. If the supplier landscape is moving, keep interfaces clean. If regulators are part of the product, hire for that before launch week, not after the first incident. The companies that win in AI-heavy physical systems will look less like pure model labs and more like operators with excellent software taste.

For incumbents, the threat is not that robots replace every driver next year. The threat is that platforms learn which pieces of your local operating knowledge can be converted into data, software, and repeatable playbooks. Once that happens, the rollout curve stops looking like a science project and starts looking like SaaS with tyres.

The sign-up form is the product test

Uber’s London interest list is small on purpose. That is what makes it useful. It asks one clean question before the city argues about everything else: when offered a robotaxi at the same price, will a Londoner tap yes?

If the answer is no, autonomy has a trust problem. If the answer is yes, the hard part begins.

Sources

- The Verge: Uber tells London to get ready for robotaxis

- Reuters via MarketScreener: Uber opens sign-ups for London robotaxis ahead of launch in months

- Uber: Uber unveils Uber Autonomous Solutions to accelerate autonomous mobility and delivery worldwide

- Wayve: Wayve secures $1.5B to deploy its global autonomy platform

- GOV.UK: Automated passenger services permitting scheme consultation

- GOV.UK: Self-driving vehicle pilot scheme information for applicants

- Uber: Wayve, Uber and Nissan announce collaboration on robotaxis

- Uber: NVIDIA to launch L4 software-driven robotaxis on Uber across 28 cities by 2028

- London Assembly: Autonomous Passenger Vehicles in London